Accounting Assignment Help With Direct Material Variances

4.7.1 Direct Material Variances

Materials constitute most important element of cost. Therefore, utmost care should be taken in purchasing and using the materials. When deviations occur between the standards specified and the actuals the following variances could be calculated:

a. Direct Material Cost Variance,

b. Direct Material Price Variance, and

c. Direct Material Usage or Quantity Variance

Let us study the above variances in detail.

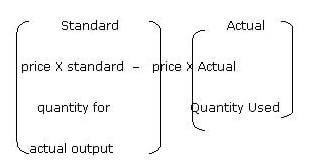

a. Direct Material Cost Variance: It is the difference between the standard cost of materials specified for the output achieved, and the actual cost of direct materials consumed. The standard cost of materials is computed by multiplying the standard price with the standard quantity for actual output. The actual cost is computed by multiplying actual price with the actual quantity used. The Direct Material Variance may be calculated with help of the following formula:

Direct Material Cost Variance = Standard Cost – for actual output Actual Cost

(DMCV)

Where,

Standard Cost = Standard Price per unit X Standard Quantity used for actual output

Actual Cost = Actual Price X Actual Quantity used.

Direct material cost variance arises due to change in price of materials or change in the quantity of material used or both. If the standard cost is more than the actual cost, the variance will be favourable and on the other hand, if the actual cost is more than the standard cost the variance will be unfavourable or adverse.

Example

Calculate Direct Material Cost Variance with the help of the following information:

Standard Output : 1600 Units

Actual Output : 2000 Units

Standard Quantity required per unit : 2 Kg.

Total Quantity actually consumed : 2400 Kg.

Standard rate per unit : $ 8 per Kg.

Actual rate per unit : $ 10 per Kg.

Solution

Direct Material Cost Variance = Standard Cost – Actual Cost

or

= $ 8 X 2 kg X 2000 kg - $ 10 X 2400kg

= $ 32000 - $ 24000

= $ 8000 (Favourable)

b. Direct Material Price Variance: Direct Material Price Variance is the difference between actual price and standard price of materials consumed. Material price variance may arise due to the following reasons:

i) Changes in the prices of materials,

ii) Uneconomical size of purchase orders,

iii) Failure to purchase materials at proper time,

iv) Fluctuations in the cost of transportation and carriage of goods,

v) Buying efficiency or inefficiency

vi) Not availing cash discounts when setting standards,

vii) Purchase of substitute material for non-availability of specified material

viii) Changes in the duty structure which is forming part of price,

ix) Inefficiency of purchase department etc.

Some of the above factors are controllable if proper care is exercised by the management. Generally, the Purchase Manager will be held responsible for material price variance. Material price variance will be calculated as follows:

Direct Material Price Variance = Actual Quantity (Standard Price – Actual Price)

= AQ (SP – AP)

If the standard price is more than the actual price, the variance would be favourable and in case the actual price is more than the standard price, it shows adverse variance. Adverse material price variance shows that unfavourable prices were paid for materials consumed and the Purchase Manager would be asked to explain the position.

c. Material Usage (Quantity) Variance: Material Usage Variance is that portion of material cost which arises due to the difference between the standard quantity specified and the actual quantity used. In other words, it is the difference between standard quantity for actual output and actual quantity, multiplied by standard price of material. The formula for material usage variance is as follows:

Material Usage Variance =

Standard Price (Standard Quantity for actual output – Actual Quantity)

MUV = SP (SQ - AQ)

This Variance will be considered favourable when standard quantity is more than actual quanity and vice versa. The production Manager will be held responsible for material usage variance. Material usage variance will arise due to the following reasons:

i) Use of sub-standard or defective materials,

ii) Carelessness in the use of materials,

iii) Use of substitute materials,

iv) Inefficient production methods,

v) Change in designs than those specified,

vi) Pilferage of material,

vii) Use of non-standard mix,

Direct Material Cost Variance is equal to the sum of Direct Material Price Variance and Material Usage Variance. Thus,

Direct Material Cost Variance = Material Price Variance + Material Usage Variance

Example

Gemini Chemical Industries provides the following information from their records:-

For making 10 kgs. Of GEMCO, the standard material requirement is

Material Quantity Rate per kg.

A 8 units $ 6.00

B 4 units $ 4.00

During April, 2004, 1000 kgs of GEMCO were produced. The actual consumption of material is as under:

Material Quantity Rate per kg.

A 750 units $ 7.00

B 500 units $ 5.00

Calculate:

a) Material Cost Variance

b) Material Price Variance

c) Material Usage Variance

Solution:

a) Material Cost Variance = Standard Cost – Actual Cost

= $ 6400 – $ 7750

= $ 1350 (A)

b) Material Price Variance

= (Standard Price – Actual Price) X Actual Quantity x Material

= ($ 6 – $ 7) 750 = ($ 4- $ 5) X 500

= $ (-1) 750 = $750 (A)

= $ 1250 (A)

y Material = ($ 4 – $ 5) X 500

y Material = ($ 4 – $ 5) X 500

= $ 500 (A)

x + y Material = $ 750 (A) + $ 500 (A) = $ 1250 (A)

c) Material Usage Variance

= (Standard Quantity for actual output – Actual Quantity) X Standard Price

= x Material + y Material

= (800 kg. – 750 kg) $ 6 + (400 kg – 500 kg) $ 4

= $ 300 (F) = $ 400 (A)

= $ 100 (A)

Verification

Material Cost Variance = Material Price Variance + Material Usage Variance

$ 1350 (A) = $ 1250 (A) + $ 100 (A)

Email Based Assignment Help in Direct Material Variances

Following are some of the topics in Standard Costing in which we provide help:

Accounting Assignment Help | Accounting Homework help | Help with Accounting | Management Accounting | Cost Accounting | Online Tutoring | Financial Accounting | Email Based Accounting Homework Help