Accounting Assignment Help With Standard Costing

4.7.2 Direct Labour Variances

The labour directly engaged in the production of a product is known as direct labour. The wages paid to such labour is known as direct wages. For example, the wages paid to a machine operator is a direct labour cost. Labour variances arise when actual labour costs are different from standard labour cost. The setting up of standard direct labour cost will depend upon the following factors:

a) Methods of Production: Standardized methods of production will be decided by studying motion study.

b) Labour time standards: The time taken by different categories of workers is known as Labour time standard it will be ascertained by using past record performance, time and motion study.

c) Labour rate standards: It refers to the expected wage rate to be paid to different categories of workers. While deciding standard labour rate past wage rates, demand and supply of labour, anticipated changes in wage rates etc. should be taken into account. The methods of wage payment like time rates or piece rates and incentive plans are also to be considered while fixing standard labour rate.

d) Different grade of labour mix: Standard proportion of different grades of labour mix is another important factor in setting standard labour cost.

Direct labour variance is the difference between the standard direct labour cost specified for the activity achieved and the actual direct labour cost incurred. It is calculated as follows:

Direct Labour Cost Variance = Standard Labour Cost – Actual Labour Cost

or

= (Std. hours X Std. Rate) – (Actual hours X Actual rate)

= (SH X SR) – (AH X AR)

Note: When the actual output differs from standard output, standard labour cost of actual output is to be worked out and then the following formula is to be applied:

DLCV = Std. cost of actual production – Actual cost

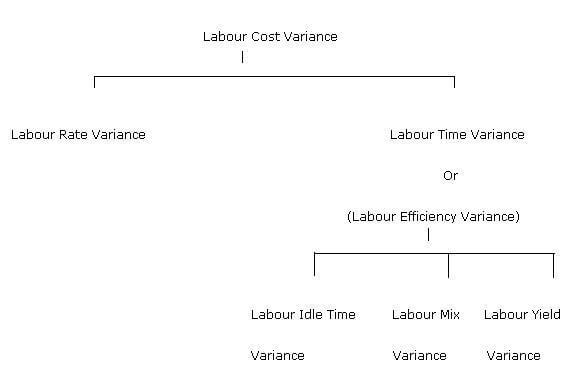

Direct Labour Cost Variance is sub-divided into:

1. Labour Rate Variance

2. Labour Efficiency Variance

Labour Efficiency or Time Variance may again sub-divided into:

a. Labour Idle Time Variance

b. Labour Mix Variance and Labour Yield Variance

The above classification may also be shown diagramatically as follows:

Labour Rate Variance

Labour rate variance is that portion of the usage variance which is due to the difference between standard rate specified and actual rate paid. It is calculated with the help of the following formula:

Labour Rate Variance = (Standard Rate – Actual Rate) X Actual Hours Paid

LRV = (SR – AR) X AHP

The variance will be favourable if actual rate is less than the standard rate and it will be adverse if actual rate is more than the standard rate. The responsibility for labour rate variance lies with the production centre. Labour rate variance is generally uncontrollable.

If the variance is due to wrong grade of labour, the responsibility lies on production foreman. Labour rate variance arises due to the following reasons:

i) Change in the basic wage rate of piece-work rate

ii) Employment of one or more workers of different grades than the standard grade

iii) Payment of more overtime than fixed earlier

iv) Higher or lower wage rates paid to casual labourers

v) Faculty recruitment and placement of workers

vi) New workers not being paid at full wage rates etc.

Labour Time Variance or Labour Efficiency Variance

Labour efficiency ratio is the difference between the standard labour hours specified for actual output and the actual hours paid for. This variance helps in controlling efficiency of workers and also labour cost. This variance can be calculated as follows:

Labour Efficiency Variance

= (Standard hours for actual production – Actual hours worked) X Standard Rate

OR

(LEV) = (SHAP – AHW) X SR

If actual time taken for doing a work is more than the specified standard time, the variance will be unfavourable and vice versa. Labour efficiency ratio arises due to one or more of the following reasons:

1) Defective machinery and equipment

2) Lack of proper supervision

3) Use of defective or non-standard materials

4) Lack of proper training to workers

5) Poor working conditions

6) Labour turnover or change over of workers from one operation to another.

7) Alterations in the methods of production

Labour efficiency variance is the responsibility of Production Manager and is similar to materials usage variance. Both these variance measure the difference in performance.

Email Based Assignment Help in Direct Labour Variances

Following are some of the topics in Standard Costing in which we provide help:

Accounting Assignment Help | Accounting Homework help | Help with Accounting | Management Accounting | Cost Accounting | Online Tutoring | Financial Accounting | Email Based Accounting Homework Help