Tnt airways and emirates skycargo sign code-share agree-ment

e

|

Contents lists available at ScienceDirect | |

| Journal of Air Transport Management | ||

| journal homepage: | ||

| a r t i c l e i n f o |

|

|---|---|

| Article history: Received 9 November 2015 Received in revised form 22 August 2016 Accepted 23 August 2016 Available online xxx |

|

| Keywords: Airline diversification Airline groups Strategic direction Vertical integration |

| 1. Introduction | core passenger business of an airline, the question arises as to what |

|---|

Corporate diversification within the airline business has a long history. Many of the first airlines were initiated as related sub-ventures by existing transport-focused organisations; such as United Airlines, which can trace its lineage to Boeing Air Transport in 1927 (Rodgers, 1996). As the industry grew and matured, Pan American World Airways came to epitomise the concept of a global aviat ion services empire, with subsidiaries such as Pan Am World

This will be investigated through a specific analysis of the Luf-thansa and Emirates Groups, both individually and comparatively. Each has been chosen due to their industry prevalence and ability to serve as emblematic representations of legacy carriers, acting as bellwethers for broader industry trends. The business units focussed upon have been chosen on the basis of the scale of their overall revenue share in each group (top 3). These units are shown

E-mail address: i (J.F. O'Connell).

0969-6997/© 2016 Elsevier Ltd. All rights reserved.

2 N. Redpath et al. / Journal of Air Transport Management xxx (2016) 1e18

| Company |

|

|---|

|

||

|---|---|---|

| Lufthansa | DLM and Travel Services | |

|

||

|

||

| Maintenance Repair and Overhaul | ||

order generate recommendations for a uniform or a non-uniform approach to vertical integration. The Strategic Scoring Method, employed for this study was based upon a selected series of stra-tegic and financial criteria employing quantifiable insights as referenced against the BCG and SWOT matrices. One overall busi-

Fig. 1. Methodology outline.

below in Table 2.

2. Data sources and methods

1 Full tables showing all business units can be made available upon request to the corresponding author i.

|

|---|

|

|

|||

|---|---|---|---|---|

| Parent company revenue growth (avg. 2009e2014) |

|

|

||

|

||||

|

||||

|

|

|||

|

||||

|

||||

|

|

|||

|

|

|||

| 2 Retain and review | 3 Invest in BU and build value | 4 Divest or leverage | ||

| 1 Consider resale or restructure |

30%. Revenue is used as a proxy for the earnings potential of the parent and as such the cash resources available to its Business

Lufthansa Group), as well as broader industry oversight (i.e. more objective view) from figures such as Giovanni Bisignani from IATA.

Business Units). historical evidence

BU Revenue Growth indicates the trend followed by the busi-

BCG Position further underpins BU market share by noting the combination of relative market share and market growth to find

to the topic of airline diversification strategy from a group, or umbrella-company viewpoint. Case-by-case analysis has been carried out in recent years (Heracleous and Wirtz, 2009; Lindst€adt and Fauser, 2004; Jones, 2007), with attention paid to their indi-

Strategic Options Available relates to the number of Strategic Options identified by the Ansoff matrix as areas for potential development e a low number of options may indicate a business unit with little potential for growth.

Average Score denotes the average of the above rankings to provide a final positioning.

hold capacity e with some then diversifying further into pure-

Interviews were conducted with a mix of experts from inside and outside the two selected Airline Groups all of which were

|

|---|

| Threat |

|

|

|

|---|---|---|---|

| Competitive rivalry | |||

| Supplier bargaining |

|

|

|

| Moderate Strong global MRO sector controlled by competitors | |||

|

Increasing dominance of online price-comparison |

|

|

| High | Launch of flydubai to tackle Air Arabia and reduce threat from other current and | ||

|---|---|---|---|

|

|

||

| Launch of Emirates Executivea | |||

| Threat of substitutes | |||

Source Author research/interviews.

ability to exhibit strength in all aspects of Porter's ‘five forces’ contract issues. Within the airline industry, evidence exists to

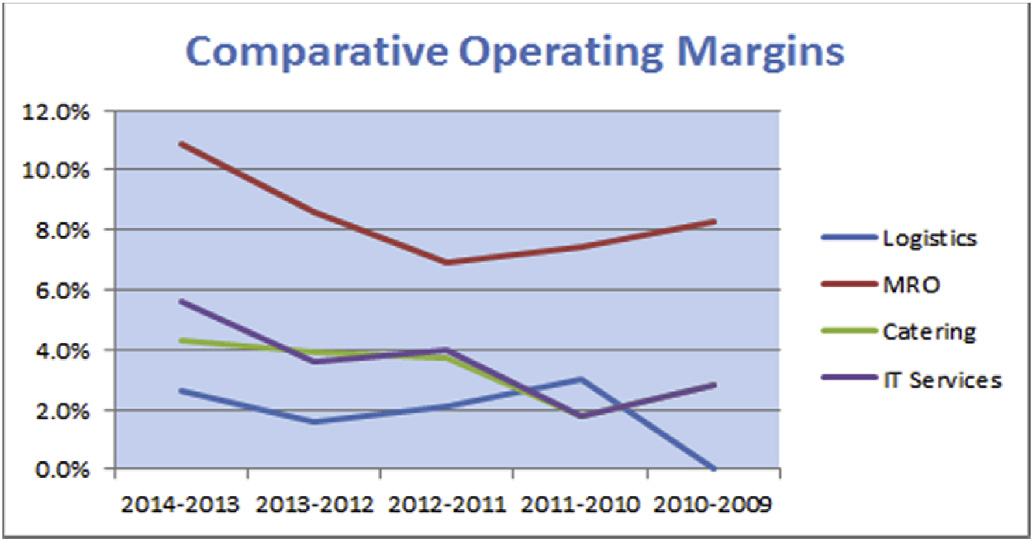

MRO serves as a useful example of a revenue stream that can provide significant tangible benefits, but also incur large costs. With the potential to represent 10e15% of an airline's operational overheads (Al-Kaabi et al., 2007; Kilpi and Ari, 2004; CAPA, 2014a,b), MRO presents a compelling case for pursuing an outsourcing strategy when viewed at face value. However, where in-demand technical competency can be married to the prospect of generating incremental revenue, in-sourcing functions such as MRO can pay notable dividends e provided the business unit is capable of supplying third parties to a meaningful degree of reve-nue generation. An example of this may be seen in Delta Airlines' investing in AeroMexico for the primary purpose of building its MRO portfolio (CAPA, 2011). Heracleous et al. (2004), Heracleous and Wirtz, 2009) highlight the notion that related diversification into higher margin sectors not only provides healthy alternative revenue streams, but also in their analysis of Singapore Airlines Engineering provide practical evidence of a business unit simulta-neously servicing the core business (Singapore Airlines), as well as

|

group-level | costs | and | reinforcing | group | ||

|---|---|---|---|---|---|---|---|

dustry. Diversification empowers airlines to avoid dependence on one product line, to achieve greater stability of profits, to make greater use of an existing distribution system and to acquire value

Where a carrier lacks the scale to profitably support its own needs and sell to third parties, the prospect of diversification may seem less attractive (Heikkil€a and Cordon, 2002); conversely a

Ansoff supports this notion, noting, “if (a firm's) diversification objective is to correct cyclic variations in demand that are charac-teristic of the industry, it would choose an opportunity that lies outside” (pg. 122, Ansoff, 1957). However, emerging trends in this market such as the encroachment of Original Equipment Manu-facturers (OEM's) will begin to erode the position of even strong providers like Lufthansa, with Airbus already predicting 25% of its revenues to be generated by MRO sales by 2020 (Aviation Week,

heavily by organisational characteristics, as well as vendor and 2012).

| 2 Personal interview with Harald Heppner, Manager Corporate Strategy, Luf- |

|---|

N. Redpath et al. / Journal of Air Transport Management xxx (2016) 1e18 5

| margin, | non-flying | subsidiaries | to | absorb | financial | risk | is |

|---|

apparent from their EBIT between 1997 and 2000 e showing that non-flying divisions almost consistently delivered a greater com-bined result than the airline itself, culminating in an average earnings ratio of approximately 2:1 against passenger operations. Arguably, had the SAir Group focussed on these types of business, rather than investing in loss-making equity airline partners such as the chronically unprofitable Sabena, then it may have been better positioned to respond to the spate of disasters that befell it between 1999 and 2001.

Looking towards the future, investment into middle-ground investments that may arguably straddle the fields of related and unrelated diversification within the air transport industry has not yet seen much academic discussion. Krishnan and Ellis (2008) note that Berkshire Hathaway serves as an example of a business with aviation interests that pursues a highly successful, yet largely un-related investment strategy. They additionally argue that compe-

| across | multiple | sectors, | consequently | increasing | consumer |

|---|

Even the cessation of trading by the headline brand arguably did not harm many of the sub-brands of the SAir Group. Many of Swissair's business units continue to be active in the marketplace, including Swissport, Gate Gourmet, Rail Gourmet, Balair (reor-ganised as Belair), Swissotel, SR Technics and Crossair (reorganised as Swiss International Air Lines).

It may be inferred from the example of the SAir Group that the often stronger earning potential of higher-margin, non-airline subsidiaries may provide greater benefits to the lower-margin airline itself, than vice versa. The integration of so-called “invis-ible assets” (Teece et al., 1997) refers to the intangible benefits reaped by marketing in a diversified business which lend them-selves to the individual survival of SAir's units, not so much for their linkage to an admittedly tarnished brand, but due to their ability to leverage existing commercial and consumer relationships built under the group's original brand umbrella.

3 Personal interview with Ram Menen, Divisional Senior Vice President, Emirates

The ability for subsidiaries to inform learning across the busi-ness is made apparent by Heracleous et al.'s (Pg 38, 2004) assertion that Singapore Airlines (SIA) benefits from a notable “transfer of learning” between subsidiaries through staff job rotation. This en-courages greater group-level oversight of the organisation, as opposed to business-unit level compartmentalisation. The net gain of employee competency and knowledge of multiple areas can be spread throughout the wider business. Support for this enhanced ability to inform the business' capabilities through cross-sharing of knowledge can be found in Day (1990), who defines the concept of

| corporate | ‘capabilities’ | as | a | “complex | bundle | of | skills | and |

|---|

Where errant corporate logic is present, a firm's need to diver-sify may be ill-informed or unable to adapt to rapidly changing market conditions. This in effect mirrors the stock-market concept of a ‘value trap’, whereby an investment may appear to be sound in isolation, but can prove toxic to a portfolio due to consistent underperformance, or in this case its inability to aid the business in relating to its marketplace, as per Porter. Ansoff also supports this notion, arguing that companies may generate new competition through diversification from strong incumbents that it is under-equipped to counter.

4. Overview and business trend analysis

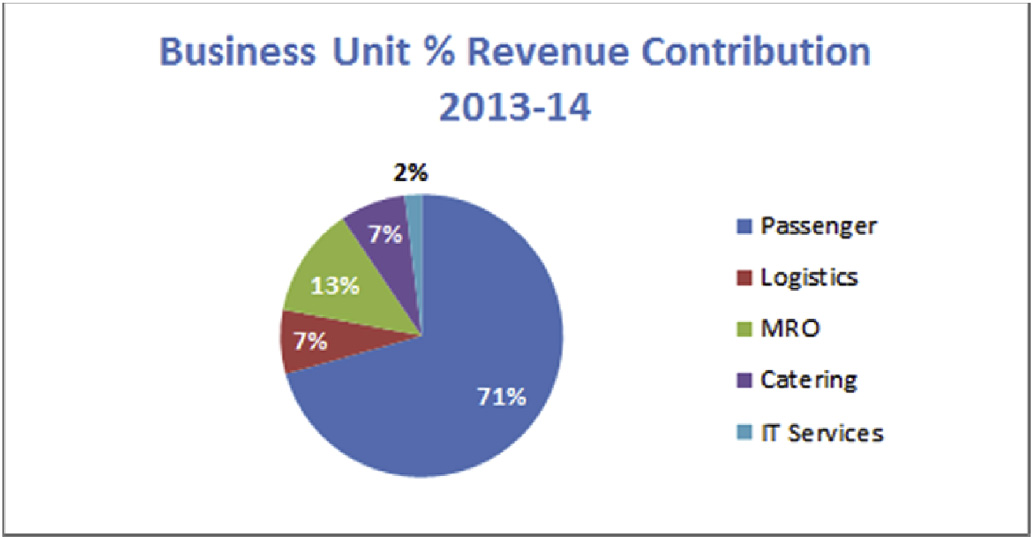

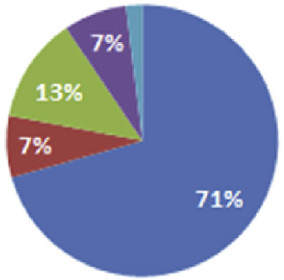

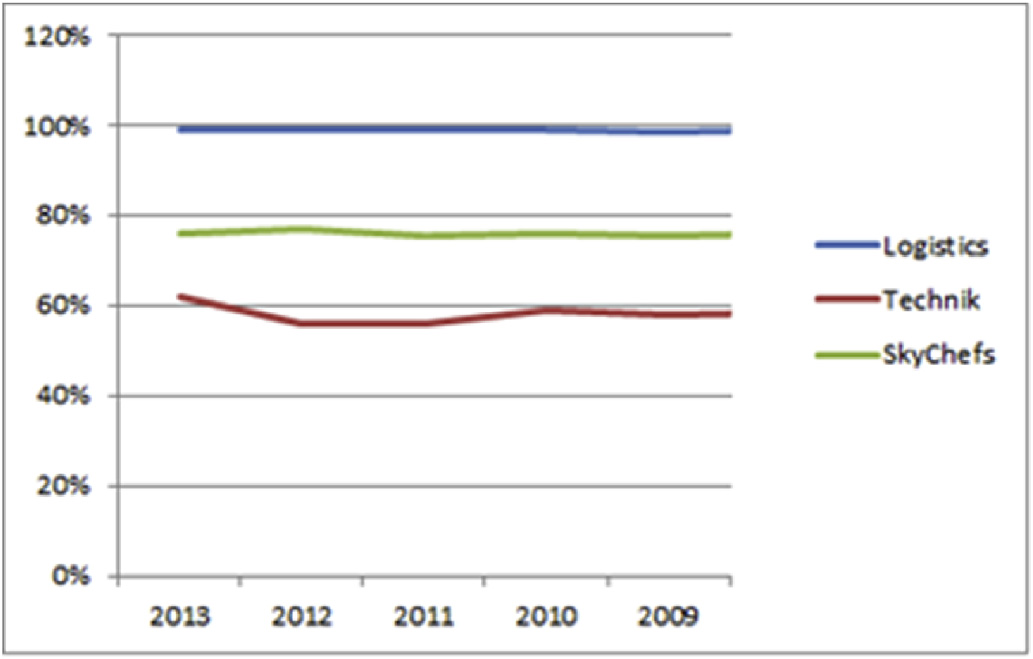

MRO initially appears to be particularly strong, but further analysis in Section 4.1.2 illustrates the underlying factors that may suggest its future could be in doubt. Indeed, headline figures for all revenue contributions require closer analysis. Whereas Fig. 4 (below) may show Logistics to have the highest percentage of external revenue (99%), it is important to note that this is achieved by default, as Logistics lacks internal trading partners. This is fol-

|

|---|

4.1.1. Logistics: business trends analysis

Cargo presents a mix of fortunes for any airline group, Laurie Berryman, Vice President UK, Emirates Airline, asserts that it is arguably one of the only diversified revenue streams available to airlines “by default”. Harald Heppner, Manager Corporate Strategy, Lufthansa, agrees, noting that cargo is an “in-built, ready-to-use

|

|---|

Source(s) Adapted from LH Group Annual Re-

ports 2013e2014.

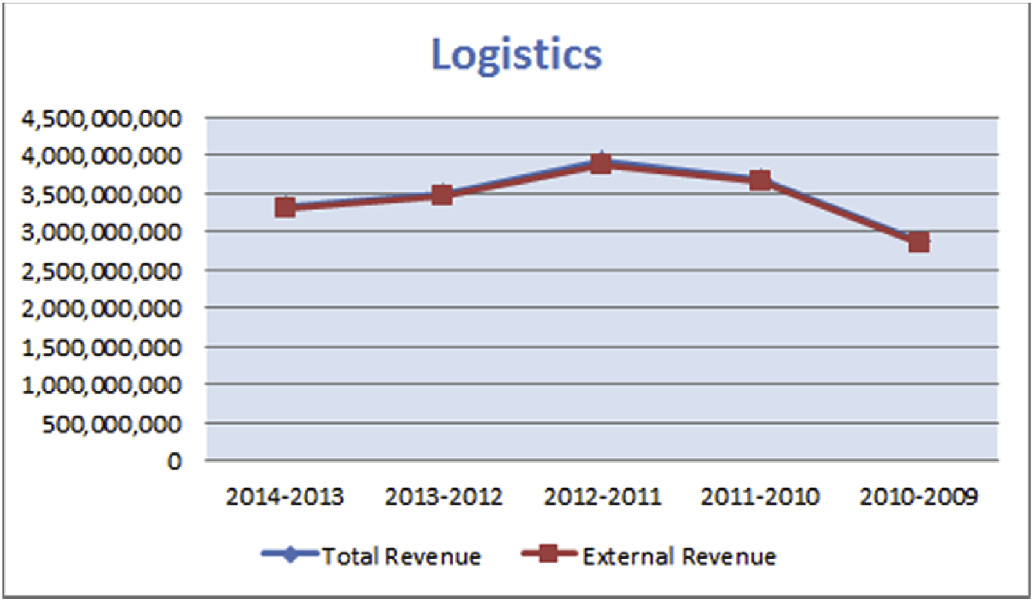

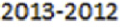

Fig. 5. Logistics revenue trend 2009e2014.7

to deliver margins arguably fails to overcome this small bonus.

Although Logistics is presently seeing a downturn and is subject

to a high degree of cyclicality, it is nevertheless able to deliver

benefits to the wider group even when its own financial prospects

are challenged e this demonstrates a particular strength of diver-

sification. IATA noted moderate growth of 1.8% in the cargo market

in 2013, with the trend expected to continue into 2014 (IATA, 2014).already possessing bellyhold capacity that would otherwise be left solely for baggage or mail transport. In spite of this low initial barrier-to-entry, it is also a notoriously challenging sector, partic-ularly due to its sharing of fuel cost with passenger operations (Holloway, 2008). Although this has the potential to cross-subsidise operations in both areas, inefficiencies inherent to the cargo arena can be difficult to overcome. Flexibility may be built into the model by introducing pure-freighter aircraft to offset gaps in the passen-ger network (Flight Global, 2013), but the costs of freighter intro-duction and operation often outweigh the benefits of leveraging bellyhold capacity if operational scale is insufficient (Morrell, 2007).

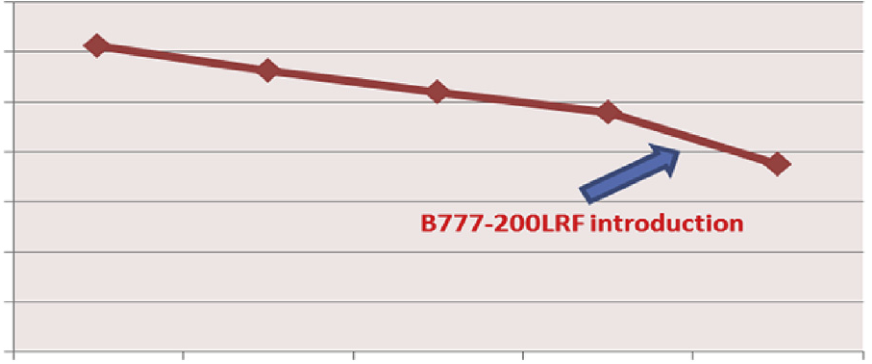

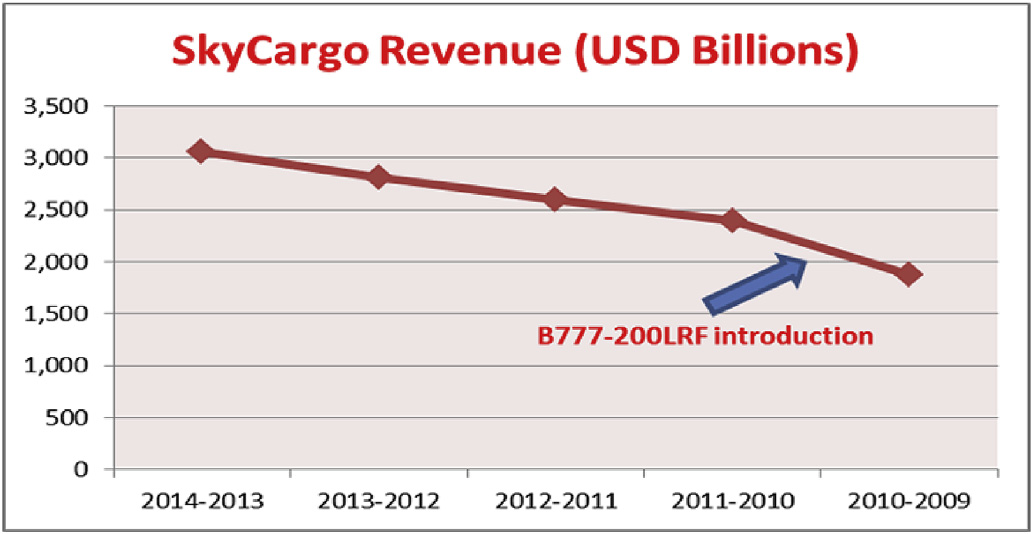

Global cargo market downturn towards 2011e2012 (Flight Global, 2013) has seen Logistics’ operating margin collapse from a 2010 high of 11.4% to a 2009 low of8%; both the respective highest and lowest of any Lufthansa Group business units. Despite scaling back pure-freighter growth plans (Flight Global, 2013), revenues recovered in 2013 to gain USD 500 million on 2009 levels, however this is still a decrease year-on-year versus 2012 (USD 3.49bn) and 2011(USD 3.9bn). A side benefit of this could be seen in the elimi-nation of competitors, particularly in the pure-freight arena, where Air France/KLM has withdrawn the majority of its fleet (CAPA, 2013a,b), although this has also benefited fast-growing competi-tors in the Arabian Gulf.

7 Logistics External Revenue (USD 3,423,850,000) contributes 99% of Total Rev-enue (USD 3,457,416,000).

|

|---|

benefits currently seen by Lufthansa. The case may be that MRO is a strong sector for businesses with existing operations, but the financial barriers to entry are high, dampening the potentially solid margins it is capable of achieving otherwise.

It is also an employee-intensive operation, requiring 20,000 staff e which despite being less than half of Passenger's requirements, does still show that it has the second lowest productivity-per-employee rate within Lufthansa Group. This is exacerbated by a costly, entrenched union structure (Irish Independent, 2013), which when combined with the OEM dilemma, may play their part in reducing the attractiveness of Technik as an investable asset in the

| Lufthansa | Group, | averaging | 8.4% | between | 2009 | and | 2013, |

|---|

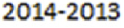

Fig. 6. Technik operating margin.

Source adapted from LH group annual reports 2009e2014.

Fig. 8. SkyChefs revenue.

|

|---|

mary competitor could be observed as a strategic threat to the as a whole.

Lufthansa Group. However, it could also represent a significant opportunity due to the potential for Lufthansa Group to sell Sky-Chefs at a time of predicted market growth,9maximising the sale value of the business unit. Equally, Lufthansa Group could miss out on the opportunity to retain a newly cost-efficient, market leading business unit poised to deliver strong returns.

To generate insight into Emirates’ strategy and the trends it is subject to, this section explains relationships between Group business units and their role in driving the Group. Revenue gen-eration will be utilised as a KPI for each unit, cross-referenced against personal interviews conducted with senior executives across the Emirates Group to form a picture of both their perfor-mance and strategic value to the Group.

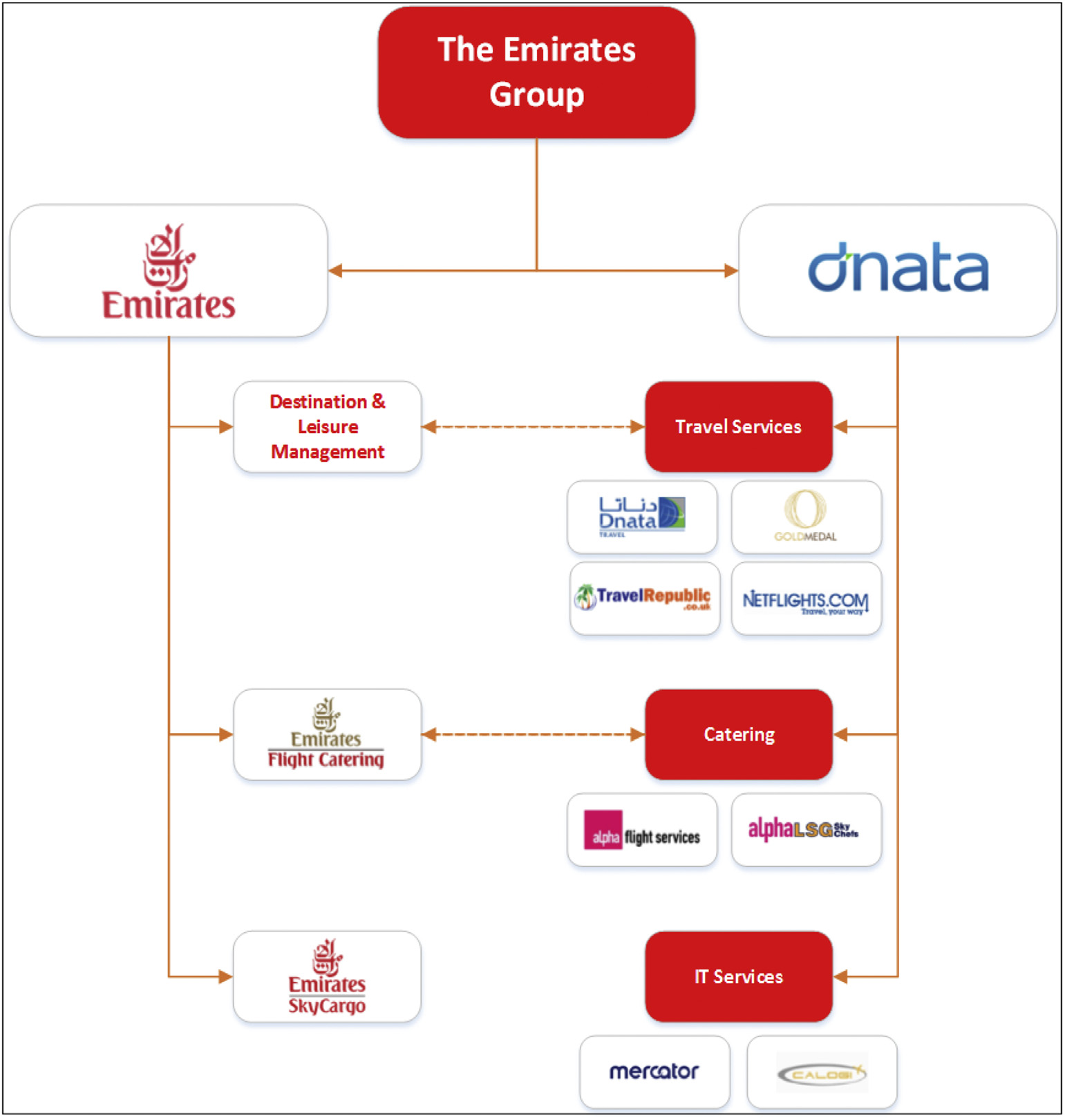

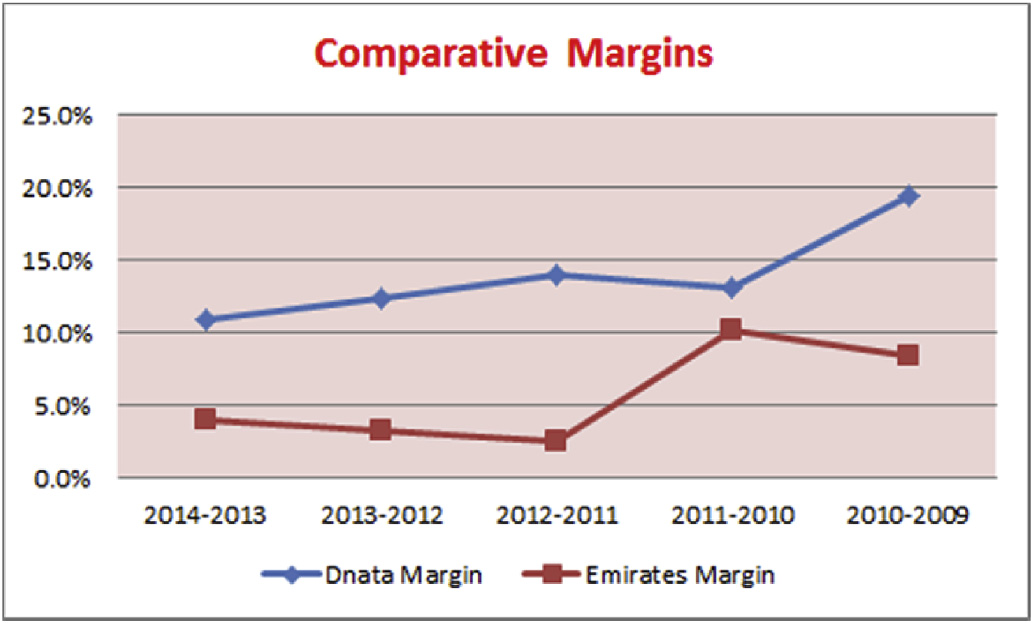

The overall split in revenue between Emirates Airline and Dnata within the group is heavily weighted towards Emirates, with Dnata accounting for an average of 8% of Group revenues between 2009 and 2014 (Figs. 10 and 11). However, Dnata's profit margin is on average more than double Emirates Airline's, at 14% versus 5.7% (Emirates Financial Reports, 2009e2014).

| with | the | carrier | dependent | on | much | of | the |

|---|

infrastructure it provides, despite not having to directly bear the cost of their operation e arguably distorting the picture. It may not

|

|---|

tive case for diversification within the Emirates Group, with a greater bias towards strategic value, rather than the financial bias evident within Lufthansa.

4.2.1. SkyCargo: business trends analysis

Emirates' SkyCargo division has achieved the remarkable feat of expanding its business in a shrinking global freight market, achieving growth “against the industry norm” (SkyCargo, 2014a,b). In 2014 it delivered 15% of group transport revenues with a total uplift of 2.3 million tonnes of cargo in (Emirates Annual Reports, 2009e2014), comfortably remaining the Emirates Group's largest non-core business unit as well as the world's largest cargo airline by available freight tonne kilometres (CAPA, 2014a,b).

Encroachment of OEMs in MRO market

Failure to acquire ‘intellectual property’

|

|---|

Fig. 10. Emirates group revenue contributions.

Airbus A380-800 versus the longer Boeing 777-300ER means that as more A380 destinations come ‘online’, overall cargo tonnage may decrease in key ports-of-call.

|

|---|

when other airlines have been reducing freighter fleets. He also

points out that this independence is seen in SkyCargo being gran-ted full P&L on freighter operations and a remit to operate as “an airline within an airline”, driving efficiency.

|

|---|

Mr. Menen argues that instead of hampering progress, the need

to propose a robust case to compete for resources has strengthened

the analytical capability of Emirates' divisions e enhancing their

business acumen (a form of ‘knowledge gain’, as discussed in Sec-

tion 2), which he believes sees significant transfer to other com-

| mercial | processes | within | the | division, | resulting | in | a |

|

|

|---|---|---|---|---|---|---|---|---|---|

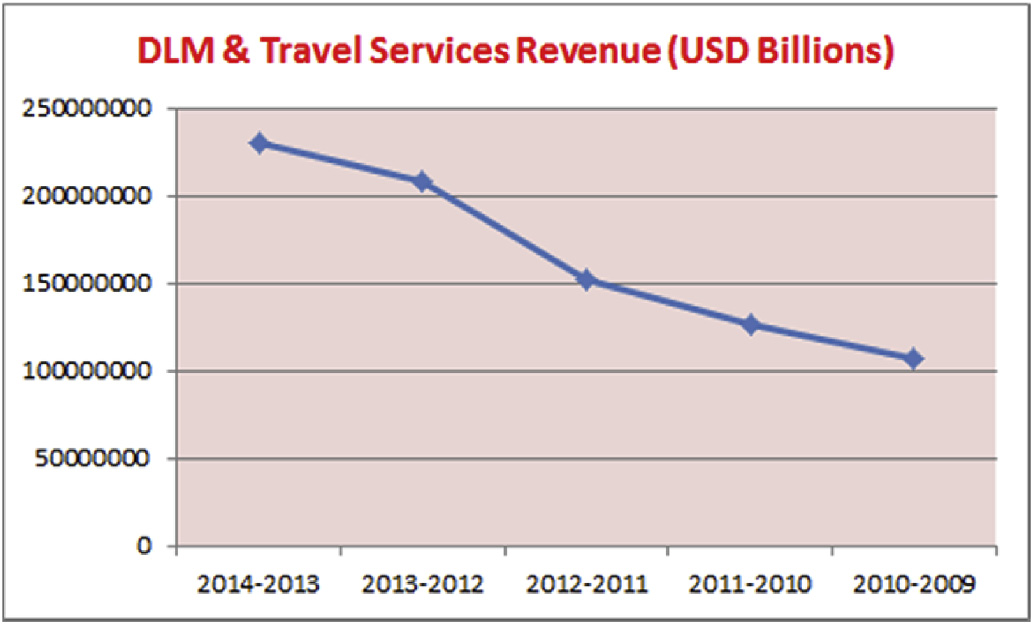

The 2014 Group Financial Report (Emirates Group Annual Reports, 2014) observes that the acquisition of Travel Republic was instrumental in driving a revenue increase from USD153m in

Fig. 13. DLM & travel services (combined) revenue.

|

|---|

The Emirates Group sees potential to segment the direction of

its DLM units, with Gold Medal continuing its role as an exclusive

facilitator of Thomas Cook's car rental and air services needs, whilstintegrating its objectives with the Emirates Group's overall aim of“continued tourism growth in the UAE” (Dnata, 2014). The end benefit to the Emirates Group can be inferred in Mr. Berryman's expectation that Gold Medal has the potential to drive larger numbers of Thomas Cook passengers to Emirates flights, as well as

| underpinning | Mr. | Prestijacopo's | comments | about | enhancing |

|---|

12 Personal interview with Laurie Berryman.

13 Catering was not reported as an individual revenue stream by the Emirates Group until the 2010e11 financial year, reflecting the acquisition of the Alpha Catering Group.

14 Personal interview with Laurie Berryman.

|

|---|

5.2. Strategic value & directionality: Lufthansa

Logistics is a ‘Cash Cow’. The downturn in the freight market has resulted in low market and business unit growth, but its high relative market share in such a market demonstrates an ability to perform against wider trends. Additionally, a fairly positive future market outlook and a reduction in competitors due to the down-turn present a healthy number of strategic options, including the ability to grow outside of Emirates SkyCargo's traffic flows. Logistics performs below the group average of a 4.3% margin, but a rein-vigorated freight market could reverse this. Exposure to risk in the form of pure-freighter operations may be seen as a drain or a bonus but trading could improve if Lufthansa turned to pure bellyhold operations, due to the sharing of costs with the passenger division. Lufthansa may wish to retain Logistics and conduct a strategic re-view of operations. However, at present the cargo market remains a solid investment, so investment and building value may be viable

5.1. Market growth and relative market share

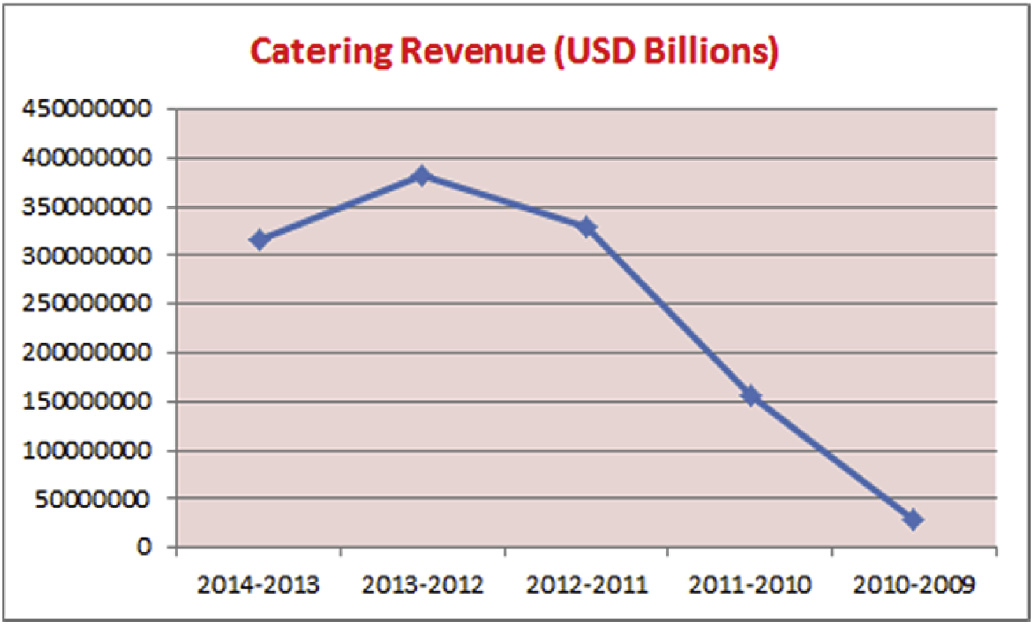

The BCG Matrix has been constructed on the basis of each BU's‘relative share’ within its own market versus the growth rate for that market.15The highest growth rate was seen in the ‘Travel Ser-vices’ sector at 12% and the lowest in Flight Catering at 2%, with relative shares falling between 100% (for market-leaders such as SkyChefs) and less than 1% (Emirates DLM) (see Fig. 15).

SkyChefs is a ‘Cash Cow’, with the potential to move into ‘Star’territory e this is due to its position as a market leader and fore-casts of highly positive growth in the catering market. This estab-lishes high potential value, which may not be fully accounted for in the rankings. The strategic benefits of controlling in-house catering operations are apparent, but the potential for sale underpins its financial value as well. However, a buyer could be Emirates, which could deliver value to an already strong competitor, diminishing the strategic attractiveness of selling the unit. Based on current market and business unit growth, it may appear to be an under-achiever, but its strong future prospects may support retention as a prudent strategic and financial option in the short term. SkyChefs sits across boundaries, with an indicative direction pointing to-wards review and investment pending a decision regarding divestment. The intangibility of future prospects precludes a higher ranking, but Lufthansa may wish to retain and leverage the up-turn of the catering market.

5.3. Strategic value & directionality: Emirates Group

14 N. Redpath et al. / Journal of Air Transport Management xxx (2016) 1e18

Table 6

Autonomy A380 vs. B777 bellyhold disparity

Broad Emirates network (Bellyhold)

Potential to acquire LSG SkyChefs

Strong market growth predicted

Alpha-LSG joint venture in UKGrowth of new suppliers (e.g. Do&Co)

Emirates' Catering unit is a ‘Dog’ which could rapidly progress to being a ‘Star’. Forecasting of a significant rebound in the catering market and the acquisition of Alpha Flight Catering (the results of which have not yet been fully realised) may serve to rapidly add financial and strategic value via increasing marketshare in a growing market. Potential acquisition of LSG SkyChefs would consolidate a position as a highly profitable market leader, but this remains only a possibility at present and cannot be fully accounted for in the rankings. To prepare for growth, Emirates may invest in

| ates | invest in | this sector e pursuing product | and market |

|

|---|

fact that both have survived market contraction and retained market leading positions may allow them to leverage this advan-tage into drawing marketshare away from weakened competitors.

|

5.4.2. Emirates |

|---|

5.4.1. Lufthansa tourism (SYTA, 2012), representing a highly fertile segment in

Market development for Lufthansa Group presents an issue in light of the fact that progression of the business may be dependent on retraction or significant review in some areas (notably MRO), as opposed to further market penetration or product and market development. However, as no Lufthansa Group business unit fell

The acquisition of LSG SkyChefs e should Lufthansa opt for sale e represents a significant gain for Emirates, however the significant capital outlay required to meet its 2012 estimated valuation of USD 1.1 billion (Morgan Stanley, 2012) and the prospect of projected market growth failing to materialise increase the risk of pursuing this option. It is nevertheless offset by the potential to move into‘Star’ territory, should acquisition prove possible and successful.

DLM and Travel Services may opt to continue growing organi-cally through its integration with Emirates Airline. Laurie Berryman notes that one of the strongest areas for growth in Emirates' port-folio has been “three and four star” travel, as opposed to Dubai's typical association with five star luxury. This growth in lower value, fed by organic volume growth in line with the carrier's ambitious expansion plans could significantly grow marketshare, contributing to its move into the ‘Star’ BCG quadrant.

| Underachiever | Weak Performer | Best in Class |

|---|

Lufthansa Logistics

|

1. Consider Sale or Restructure | |||

|---|---|---|---|---|

| 3. Invest in BU and Build Value |

Lufthansa Technik

|

1. Consider Sale or Restructure | 4.Divest or leverage | ||

|---|---|---|---|---|

| 3.Invest in BU and Build Value |

|

1. Consider Sale or Restructure |

|

||

|---|---|---|---|---|

| 3. Invest in BU and Build Value |

|

1. Consider Sale or Restructure | 2.Retain and Review |

|

|

|---|---|---|---|---|

|

1. Consider Sale or Restructure | 2. Retain and Review |

|

|

|---|---|---|---|---|

| 3.Invest in BU and Build Value |

| 1. Consider Sale or Restructure |

|

|

||

|---|---|---|---|---|

This study has uncovered that firstly the strategic value of a diversified portfolio of related, non-core subsidiaries can be illus-trated by Emirates' investment in Travel Services as a cost-effective method of feeding its core passenger transport business through exercising greater end-to-end control over the consumer journey. In the case of LSG SkyChefs, the Lufthansa Group informs strategic value somewhat differently. Despite LSG primarily adding financial value to the group, it also acts as a strategic asset when the issue of divestment to a major competitor is considered. As such, the stra-tegic value of a business unit may be defined in different ways, dependent upon diverging trends and approaches in each com-pany; that secondly an upturn in the global catering market, a downturn in in-house MRO operations at the hands of OEM's and steady growth in the travel services and cargo markets have all been revealed as external drivers of airline group performance; and

However, a weak market outlook for Technik and uncertainty over SkyChefs' future with the Group may cast some doubt on Lufthansa continuing as a widely-diversified business. SkyChefs in particular must be handled with care, due to potential to contribute signifi-cantly to the Group's strategic and financial positioning. Lufthansa's bias towards financial value over strategic value is indicative of its squeezed market position and catering to shareholders, but it must be careful not to divest or retract from sectors with weaker margins that are strategically crucial to supporting core-functions (such as Cargo). Divestment of business units may not be a wise option for Lufthansa at present unless its need to generate cash becomes more pressing. Nevertheless, this research points to a clear need for a review of strategic options available to each business unit and the pursuit of greater efficiencies in tandem with investment in prod-uct and service development. It is crucial that Lufthansa's business units keep abreast of market trends to ensure their continued viability, as in some areas e particularly Technike it is in danger of

|

|---|

further investment to continue driving growth both within the

|

|---|

|

|

|---|

The research is limited by a lack of disaggregate financial data, which prevented to the development of some comparable KPI's (e.g. ROCE). Further data likely to be unavailable for public analysis (e.g. factors informing goodwill or amortisation of assets) would require assessment, which may reveal further underlying value in retention or sale, but is not published by either group. Additionally, the Emirates Group does not publish business unit profitability statements, precluding a more in-depth analysis of its operations. As such, rankings and final assessment have produced indicative conclusions only. Interrogation into the drivers of low cost carrier

| diversification | (e.g. | the | Easy | Group) | would | provide | further |

|---|

industry-level insights. Analysis of all business units operated by

e.

AMA, 2010. What Makes Brands Elastic? Available online at:

Aviation Week, 2014a. Dubai World Central Move in 2020 Not Impossible, Says Emirates President. Available online at: (accessed 15.06.14.).

Aviation Week, 2014b. New Volume Rules Change MRO Capability Investments.

Boeing World Air Cargo Forecast, 2013. Commercial Market Outlook: Air Cargo.

| Available | online | at: |

|---|

(23/06/14).

| online | at: |

|---|

CAPA, 2013b. Delta Airlines Pledges Profitability for its Trainer Oil Refinery Business in 2014. Available online at: ii(04/06/14).

CAPA, 2014a. Asian Air Cargo Overview: Different Profiles for Major Freight Airlines

i (accessed 05.07.14.).

CAPA, 2014b. Unit Cost Analysis of Emirates, IAG & Virgin; about Learning from a New Model, Not Unpicking it. Available online at: e

Lufthansa Group Annual Report, 2013. Available online at: i.

Lufthansa Group Annual Report, 2014. Available online at: i.

Dnata, 2014. Dnata Acquires UK-based Travel Company, Gold Medal Group. Avail-

able online at:

online at: Morrell, P., 2007. Air Cargo Economics. Available online at:

Emirates

(accessed 12.05.14.).online at: l DFNI Online, 2012. Alpha LSG Merger Gets Green Light. Available online at:

(accessed 15.06.14.).

ie.

e.

Market. According to New Report by Global Industry Analysts, Inc. Available

e. online at: l

.

SkyCargo, 2014a. Emirates SkyCargo Completes Another Remarkable Year. Available online at:

| online | at: |

|---|

i. Jones, P., 2007. Flight Catering. Behr’s Verlag, Hamburg. Chpt, 1,4,1, 39e55, available

LSG SkyChefs, 2014. Available online at: . .

e.

ie.

e.

Travel Weekly, 2012. Travel Republic Sold. Available online at: