The the expense column includes salaries and wages

Accounting 2000 Chapter 4 Class Notes 1. Explain the accrual basis of accounting and the reason for adjusting entries.

2. Prepare adjusting entries for deferrals.

► Revenues are recognized when services are performed, even if cash was not received. (rendered means revenue) ► Expenses are recognized when incurred, even if cash was not paid. (is GAAP)

Cash-Basis Accounting

► Revenues are recognized only when cash is received.► Expenses are recognized only when cash is paid.

Suppose that Fresh Colors paints a large building in 2019. In 2019, it incurs and pays total expenses (salaries and paint costs) of $50,000. It bills the customer $80,000, but does not receive payment until 2020.

Prepare income statements using the cash basis:

|

0 | $80,000 | $80,000 |

|

($50,000) | 0 | ($50,000) |

| ($50,000) | $80,000 | $30,000 |

Adjusting Entries

Page 2 of 26

Accounting 2000 Chapter 4 Class Notes Types of Adjusting Entries

| DEFERRALS |

|---|

|

|---|

What is the needed adjustment? ($2,500 - $1,000 = $1,500) This is the amount “used up”

Basic Analysis:

| Assets | = | Liabilities | + | Stockholders’ Equity | ||

|---|---|---|---|---|---|---|

| Revenues | - | Expenses | ||||

| Supplies | Supplies Expense | |||||

| -$1,500 | -$1,500 | |||||

Page 4 of 26

| Assets | = | Liabilities | + | Stockholders’ Equity | ||

|---|---|---|---|---|---|---|

| Revenues | - | Expenses | ||||

| Prepaid Insurance | Insurance Expense | |||||

| -$50 | = | -$50 | ||||

Post-Adjustment Tabular Analysis:

BALANCE SHEET Income Statement

| $15,200 | $1,000 | $550 | $5,000 | = | $5,000 | $2,500 | $1,200 | + | $10,000 | -$6,450 |

|---|

Page 5 of 26

Accounting 2000

is known as depreciation.

Depreciation is an allocation concept not a valuation concept.

What is the needed adjustment? $480 / 12 = $40

Basic Analysis:

Accounting 2000

Chapter 4 Class Notes

| A | Supp | Prepd | A/D | BALANCE SHEET | + |

|

|

|||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Common | ||||||||||||||||||

| Retained Earnings | ||||||||||||||||||

| Stock | ||||||||||||||||||

| = Notes | Unearn | |||||||||||||||||

| Revenue | - |

|

- | |||||||||||||||

| $15,200 |

|

Ins | $5,000 | $0 | Pay | + | $10,000 | +$10,000 | -$6,450 | -$500 | ||||||||

| $550 | = | $5,000 | $2,500 | $1,200 | ||||||||||||||

| 3 | $15,200 |

|

$550 | $5,000 | -$40 | = | $5,000 | $2,500 | $1,200 |

|

-$40 | -$500 | ||||||

| -$40 | ||||||||||||||||||

| $10,000 | -$6,490 | |||||||||||||||||

| $8,700 | $10,000 | |||||||||||||||||

2. Unearned Revenues

Example:

Page 7 of 26

Basic Analysis:

| A | Prep |

|

A/D | = |

|

Unearn | + | Common | + | Service | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Retained Earnings | ||||||||||||||||||

|

= |

|

||||||||||||||||

| - | - | |||||||||||||||||

| $15,200 | Ins | $5,000 | -$40 | = |

|

+ |

|

+$10,000 | -$6,490 | -$500 | ||||||||

| $1,000 | $550 | $5,000 | $2,500 | $1,200 | ||||||||||||||

| = | -$400 | |||||||||||||||||

| 4 | $15,200 | $1,000 | $550 | $5,000 | -$40 | = | $5,000 | $2,500 | $800 | + | $10,400 | -$6,490 | -$500 | Revenue | ||||

| $8,300 | ||||||||||||||||||

| $21,710 | ||||||||||||||||||

Accounting 2000

Chapter 4 Class Notes

1. Revenues for services performed but not yet received in cash or recorded are called Accrued Revenue. 2. Expenses incurred but not yet paid in cash or recorded are called Accrued Expenses.

Basic Analysis:

| Assets | = | Liabilities | + | Stockholders’ Equity | ||

|---|---|---|---|---|---|---|

| Revenues | Expenses | |||||

| Accounts Receivable | ||||||

| +$200 | = | +$200 | ||||

Page 9 of 26

| $8,300 | $10,000 | - | -$500 |

|---|

$6,490 $21,910 $21,910

2. Accrued Expenses

Accounting 2000

Chapter 4 Class Notes

| Assets | = | Liabilities | + | Stockholders’ Equity | ||

|---|---|---|---|---|---|---|

| Revenues | - | Expenses | ||||

| Interest Payable | ||||||

| = | +$50 | -$50 | ||||

BALANCE SHEET Income Stmt

Ins

| A | 15,200 | 200 | 1,000 | 550 | 5,000 | -40 | = | 5,000 | 2,500 |

|

800 | + | +10,600 | -6,490 | -500 | ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| = | -$50 | ||||||||||||||||

| 6 | 15,200 | 200 | 1,000 | 550 | 5,000 | -40 | = | 5,000 | 2,500 | 800 | 10,600 | -6,540 | -500 |

|

|||

| $8,350 | 10,000 | ||||||||||||||||

| $21,910 |

|

||||||||||||||||

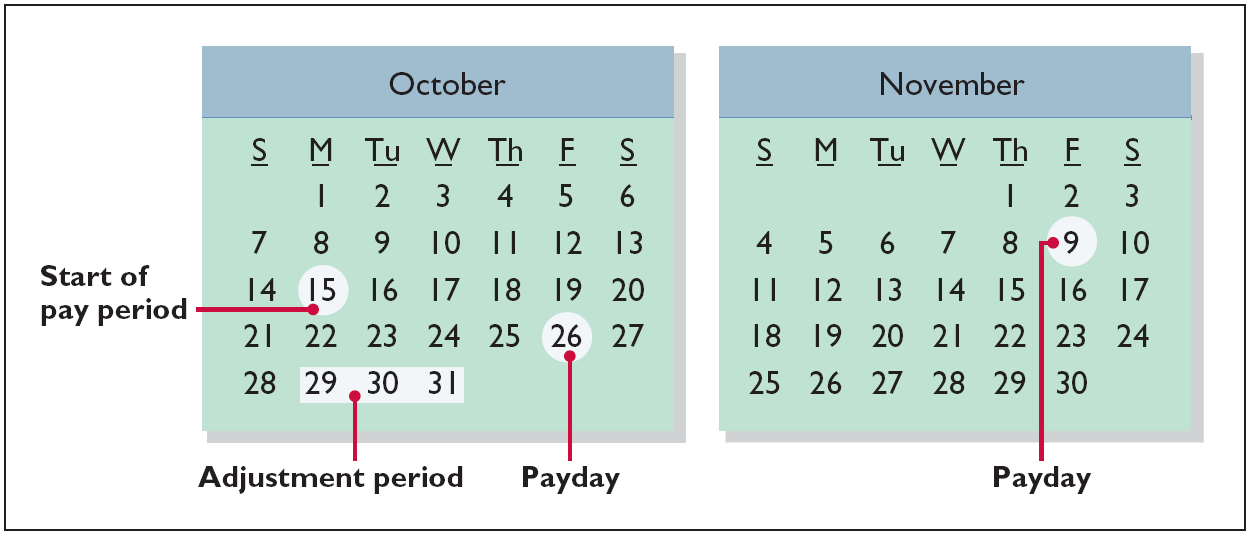

Example (Salaries):

Sierra Corporation last paid salaries on October 26; the next payment of salaries will occur on Nov. 9. The employees receive total salaries of $2,000 for a 5-day work week, or $400 per day. Thus, accrued salaries at October 31 are $1,200

Accounting 2000

Chapter 4 Class Notes

| Assets | A/R | Supp | Prep | A/D | = |

|

|

Une | + | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

||||||||||||||||||

|

Retained Earnings | |||||||||||||||||

| = | Rev | - | - | |||||||||||||||

| 15,200 | 200 | 1,00 | 5,000 | -40 | = |

|

|

Pay | Rev | + | 10,000 | 10,600 | -6,540 | |||||

| 550 | 5,000 | 2,500 | 50 | 800 | ||||||||||||||

0

| $21,910 | $9,550 | $21,910 | 10,000 | 10,600 | -7,740 |

|

|---|

|

||

|---|---|---|

Prepare Financial Statements - Companies can now prepare financial statements directly from the details provided in the tabular summary of transactions and adjustments.

Accounting 2000

Chapter 4 Class Notes

Chapter 4 class problems

3. Purchased dental equipment on January 1 for $80,000, paying $20,000 in cash and signing a $60,000, 3-year note payable (interest is paid each December 31). The equipment depreciates $400 per month. Interest is $500 per month.

4. Purchased a 1-year malpractice insurance policy on January 1 for $24,000.

Instructions

Prepare the adjustments on January 31 and record them in the tabular summary that follows.

Expense

| A3 | -$400 | -$400 | Depreciation |

|---|

| A4 | -$2,000 | Insurance |

|---|

Expense

A1 - Insurance expires at the rate of $450 per month.

A2 - A count of supplies shows $1,050 of unused supplies on May 31.

Page 19 of 26

| Supp | Prep | Land | Bldgs | A/D | Equip | A/D | = | Sal | Unear | Mort | + |

|

+ |

|

Div | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Cash | = | Acct | Int | Retained Earnings | |||||||||||||||||

| Rev | - | - | |||||||||||||||||||

| Pay | Pay |

|

|

||||||||||||||||||

1

| A |

|

-1550 |

|---|

| A | +!80 | -180 |

|---|

5

| A | +900 | -900 |

|---|

6

Page 20 of 26