The hst has replaced the gst and the pst

Business and Professional

|

|---|

U se this guide if you are a sole proprietor, an unincorporated individual or a partner in a

partnership, that is a business person,or a professional. It will help you calculate the business or professional income to report on your 2014 income tax return. Self-employed commission salespersons should also use this guide to determine the income to report for 2014.If you are blind or partially sighted, you can get our publications in braille, large print, etext, or MP3 by going

to www.cra.gc.ca/alternate. You can also get our publications and your personalized correspondence in these formats by calling 1-800-959-5525.Unless otherwise noted, all legislative references are to the Income Tax Act and the Income Tax Regulations.

|

|---|

| Page | Page | ||||

| Definitions ........................................................................... | 5 |

|

36 | ||

| Chapter 1 – General information ..................................... | 6 |

|

36 | ||

| 37 | |||||

| Business and business income ........................................... | 6 | ||||

| 37 | |||||

| How to report your business income ................................ | 7 | ||||

| 37 | |||||

| Business records ................................................................... | 7 | ||||

| 37 | |||||

| Instalment payments ........................................................... | 9 | ||||

|

38 | ||||

| Dates to remember .............................................................. | 9 | ||||

|

38 | ||||

| 10 | 38 | ||||

| 38 | |||||

| GST/HST registration ......................................................... | 10 | ||||

|

38 | ||||

| The GST/HST Registry ....................................................... | 10 | ||||

|

38 | ||||

| What is a partnership? ........................................................ | 10 | ||||

| 39 | |||||

| Investment tax credit ........................................................... | 12 | ||||

| 39 | |||||

| Chapter 2 – Income from a business or a profession.... | 12 | 39 | |||

| Sole proprietorships ............................................................ | 12 | 48 | |||

| Partnerships .......................................................................... | 12 |

|

48 | ||

|

48 | ||||

| 13 | |||||

| 48 | |||||

| Identification ........................................................................ | 13 | 48 | |||

| Internet business activities ................................................. | 13 | Sole proprietor – Sale of eligible capital property in | 49 | ||

| Part 1 – Business income ..................................................... | 14 |

|

|||

| Part 2 – Professional income .............................................. | 14 |

|

49 | ||

| Part 3 – Gross business or professional income ............... | 15 | ||||

| Part 4 – Cost of goods sold and gross profit .................... | 16 | 50 | |||

| 51 | |||||

| Chapter 3 – Expenses .......................................................... | 19 | ||||

| Current or capital expenses? .............................................. | 19 | 52 | |||

| Part 5 – Net income (loss) before adjustments ................. | 20 |

|

56 | ||

| Part 6 – Your net income (loss) .......................................... | 30 | ||||

|

56 | ||||

| Details of other partners ..................................................... | 31 | ||||

| 56 | |||||

| Details of equity ................................................................... | 31 | ||||

| Authorizing online access for employees and | |||||

| Chapter 4 – Capital cost allowance (CCA) ..................... | 32 | 56 | |||

| What is CCA? ....................................................................... | 32 | 56 | |||

| Available for use rules ........................................................ | 32 | 56 | |||

| How much CCA you can claim ......................................... | 32 |

|

57 | ||

| How to calculate your CCA ............................................... | 33 | ||||

|

57 | ||||

| 33 | |||||

| 57 | |||||

| 33 | 57 | ||||

|

|||||

|

57 | ||||

| 33 | |||||

| 57 | |||||

| 34 | |||||

| 57 | |||||

|

35 | ||||

|

57 | ||||

| 35 | |||||

| 57 | |||||

| 36 | |||||

| 57 | |||||

|

36 | ||||

|

57 | ||||

| 36 | |||||

| 36 | 58 | ||||

| www.cra.gc.ca | |||||

Arm’s length – Relationship or transaction between persons who act in their separate interests.

■the time the property is first used by the claimant to earn income; and

■the time the property is delivered or is made available to the claimant and is capable of producing a saleable product or service.

■for a building, soft costs (such as interest, legal and

accounting fees, and property taxes) related to the period you are constructing, renovating, or altering the building, if these expenses have not been deducted as current expenses.Capital cost allowance (CCA) – the deduction you can claim over a period of several years for the cost of

depreciable property, that is, property that wears out or becomes obsolete over time such as a building, furniture, or equipment, that you use in your business or professional activities.However, a non arm’s length relationship might also exist between unrelated individuals, partnerships, or

corporations, depending on the circumstances. For more information, see the definition for “arm’s length” on page 5.Motor vehicle – an automotive vehicle designed or adapted for use on highways and streets. A motor vehicle does not include a trolley bus or a vehicle designed or adapted to be operated only on rails.

■a motor vehicle you bought to sell, rent, or lease in a motor vehicle sales, rental, or leasing business;

■a motor vehicle (except a hearse) you bought to use in a funeral business to transport passengers;

www.cra.gc.ca 5

Proceeds of disposition - usually the amount you received or will receive for your property. In most cases, it refers to the sale price of the property. This could also include compensation you received for property that has been destroyed, expropriated, or stolen.

| Chapter 1 – General information |

|---|

|

Business and business income

If you sell gift cards or certificates, you must report, as business income, the amounts received from the sale on the date they are sold. A business may choose to calculate a reserve as a deduction against this income. A reserve is the amount of gift cards or certificates that you anticipate will be redeemed after the end of your fiscal year. A reserve amount that is deducted against business income in one year must be added back to business income the following year. It is your choice whether you calculate a reserve.

Do not collect the goods and services tax/harmonized sales tax (GST/HST) when a gift card or certificate is sold. When a customer uses a gift card or certificate as payment for a product or service, calculate the GST/HST on the total price of the item or service. Deduct the amount of the gift card or certificate from the amount the customer owes.

■a manufacture;

■an undertaking of any kind; and

Notes

Include all your income when you calculate it for tax purposes. If you do not report all your income, you may be subject to a penalty of 10% of the amount you did not report after your first omission.A different penalty may apply if you knowingly or

under circumstances amounting to gross negligence participate in making a false statement or an omission on your income tax return. This penalty is 50% of the tax attributable to the omission or the false statement

(minimum $100).A. We look at each case on its own merits. Generally, we consider your business to have started when you begin some significant activity that is a regular part of the business or that is necessary to get the business going.

For example, suppose you decide to start a

merchandising business and you buy enough goods for resale to start the business. At this point, we would consider the business to have started. Usually you can deduct the expenses you incur for the business from that date. You could still deduct the expenses even if, despite all your efforts, the business ended.

How to report your business income

Fiscal period

If you filed Form T1139 with your 2013 income tax return, generally you have to file that form again for 2014.

Accrual method

Incur usually means you either paid or will have to pay the expense.

Income from professional activities is business income. Therefore, you report it using the accrual method.

■deduct expenses in the fiscal period you pay them.

Business records

Benefits of keeping complete and organized records

These are some of the advantages you might benefit from when you keep complete and organized records:

■budget, spot trends in your business, and get loans from banks and other lenders; and

■prevent problems you may run into if we audit your income tax returns.

Keep track of the gross income your business earns. Gross income is your total income before you deduct any

expenses, including those associated with the goods sold. Your income records should show the date, amount, and source of the income. Record the income whether you received cash, property, or services. Support all income entries with original documents. Original documents include sales invoices, cash register tapes, receipts, bank deposit slips, patient cards, fee statements, and contracts.www.cra.gc.ca 7

| 1 | Date | Particulars |

|

|

|||||

|---|---|---|---|---|---|---|---|---|---|

| July 1 | Daily sales | ||||||||

| 146.00 | 27.00 | 173.00 | 8.65 | 13.84 | 10.00 | ||||

| 2 | July 2 | Daily sales | 167.00 | 36.25 | 26.00 | 177.25 | 8.86 | 14.18 | 32.40 |

| 3 | July 3 | Daily sales | 155.02 | 19.95 | 10.01 | 164.96 | 8.25 | 13.20 | |

| 4 | July 4 | Daily sales | 147.00 | 29.95 | 176.95 | 8.85 | 14.16 |

** If you sell to a resident in one of the participating provinces, the HST replaces the GST and the PST. For more information on the HST, see Guide RC4022, General Information for GST/HST Registrants.

On July 1, you examine the sales invoices and cash register tapes. You find that you had cash sales of $146 and sales on account of $27. In the sales journal, you record the cash sales in column 1 and the credit sales in column 2. Since there were no merchandise returns on July 1, leave column 3 blank. Column 4 then shows the total of your cash sales and your credit sales minus any merchandise returned for the day. In columns 5 and 6, show the total GST and PST you charged on your sales.

■the name and address of the seller or supplier;

■the name and address of the buyer;

■a full description of the goods or services; and

■the vendor’s business number if they are a GST/HST registrant.Example

The following expense journal is an example of how to record your expenses for the month of July:

| 8 | www.cra.gc.ca |

|---|

A. When you buy something, make sure the

seller

describes the item. However, sometimes that is not possible, as with a

cash register tape. In this case, you should write what the item is on

the receipt or in your expense journal.

Q. What should I do if a supplier does not want to give me a receipt?

Keep your records and related vouchers for the length of time specified below for your situation:

■if you file your income tax return on time, a minimum of six years after the end of the tax year to which they relate;

These retention periods do not apply to certain records. For more information, see Information Circular IC78-10, Books and Records Retention/Destruction.

If you want to destroy your records and related vouchers before the

minimum six-year period is over, you must first get written permission

from your tax services office. To do this, either use Form T137,

Request for Destruction of Records, or prepare your own written

request. For more

information, or go to www.cra.gc.ca/records.

You may have to pay interest and a penalty if you do not pay the full instalment amount you owe on time.

Note

When a due date falls on a Saturday, a Sunday, or a public holiday recognized by the CRA, we consider your instalment payment to be paid on time if we

receive it or if it is postmarked on the next business day.April 30, 2015 – Pay any balance owing for 2014 by this date. Also, file your 2014 income tax return if the

expenditures of the business are mainly the cost or the capital cost (see “Definitions” on page 5) of tax shelter investments.June 15, 2015 – Make your second 2015 instalment payment by this date. Also, file your 2014 income tax return by this date if you have self-employment income or if you are the spouse or common-law partner of someone who does, unless the expenditures of the business are mainly the cost or the capital cost of tax shelter investments. Remember to pay any balance owing by April 30, 2015, to avoid interest charges.

www.cra.gc.ca 9

Employment insurance (EI) premiums on self-employed income

Remember to claim the corresponding provincial or territorial non-refundable tax credit, on line 5829 of your provincial or territorial Form 428.

For more information, visit www.servicecanada.gc.ca.

For more information on the GST/HST, go to

www.cra.gc.ca/gsthst. For more information on who is

required to be registered, see the GST/HST Memoranda Series,

2-1 Required registration.

The GST/HST Registry

■whether the relationship is a partnership;

■the special rules about capital gains or losses and the recapture of CCA that apply when you transfer properties to a partnership;

A limited partnership is a partnership that gives its

partners limited responsibilities that are similar to those given to shareholders of a corporation. A limited partner’s liability as a partner of the partnership is, like its name implies, limited. A general partner, on the other hand, has unlimited liability.Reporting partnership income

For the following, the loss carry-forward period is 20 years:

■non-capital losses, farm losses, restricted farm losses, and life insurer’s Canadian life investment losses incurred; and

A partnership that carries on a business in Canada, or a Canadian partnership with Canadian or foreign operations or investments, has to file a T5013 partnership information return for each of its fiscal periods if:

■at the end of the fiscal period, the partnership has an absolute value of revenues plus an absolute value of expenses of more than $2 million, or more than $5 million in assets; or

–the Minister of National Revenue requests one in writing.

For more information about the partnership information return, go to

www.cra.gc.ca/partnership or see

Guide T4068, Guide for the Partnership Information Return (T5013

Forms).

Eligible capital expenditures

A partnership can own eligible capital property and deduct an annual

allowance. Any income from the sale of eligible capital property the

partnership owns is income of the partnership. For more information

about eligible capital expenditures, see Chapter 5 beginning on page

48.

GST/HST rebate for partners

–you deducted from your share of the partnership income on your income tax return.

However, special rules apply if the partnership reimbursed you for those expenses.

For example, if in 2014 you receive a GST/HST rebate for the 2013 tax year (on your 2013 notice of assessment) you have to include the amount of the rebate on your income tax return for 2014:

■Report the amount of the GST/HST rebate for partners that relates to eligible expenses other than CCA on line 9974 in Part 6 of your Form T2125, Statement of Business or Professional Activities.

The following are his 2014 motor vehicle expenses for which he did not receive any allowance or reimbursement:

$3,150.84 × (5/105) = $150.04

When filing his 2015 income tax return, he will

include $150.04 on line9974 in Part6 on page 3 of his 2015Form

T2125, Statement of Business or Professional

Activities.

An investment tax credit lets you subtract, from the taxes you owe,

part of the cost of some types of property you acquired or expenditures

you incurred. You may be able to claim this tax credit in 2014 if you

bought qualifying

property, incurred qualified expenditures, or were

allocated renounced Canadian exploration expenses. You may also be able

to claim the credit if you have

unused investment tax credits from years before 2014. For more

information about investment tax credits, see

Form T2038(IND), Investment Tax Credit (Individuals).

Apprenticeship job creation tax credit

Employers who carry on a business in Canada, other than a child care services business, can include a non-refundable amount in their investment tax credit calculation for each new child care space they create in a licensed child care facility they operate for the benefit of the children of their employees. This non-refundable amount is equal to the lesser of the following amounts:

■$10,000 per child care space created; or

If you are a sole proprietor, you must complete all the applicable areas and lines on Form T2125, Statement of Business or Professional Activities.

Partnerships

12 www.cra.gc.ca

■If you did not make any adjustments to the amount in box 116, box 120, or box 122 of your T5013 slip, the amount you enter on line 9946 will be the same as the amount you entered on line M.

■Complete the “Other amounts deductible from your share of net

partnership income (loss)” chart on page 3 to claim any expenses that

the partnership did not

reimburse you for and any other deductible amounts. Also, complete the

“Calculation of business-use-of-home expenses” chart if applicable. For

more information, see page 31.

■Complete the “Details of other partners” chart on page 4.

However, we will continue to accept other types of financial statements.

If you have both business and professional income,

you have to complete a separate Form T2125 for each.

You also have to complete a separate form for each business or

professional activity you have, if you have two or more

of either. For more information, see Interpretation

Bulletin IT-206, Separate Businesses.

Indicate the period your business year covered, which is your fiscal period. For an explanation of fiscal period, see page 7.

Enter the six-digit industry code that corresponds to your business from the appendix beginning on page 52.

Note

Tax shelter numbers are used for identification purposes only. They do not guarantee that taxpayers are entitled to receive the proposed tax benefits.

■ By selling goods and/or services on your own page(s) or site(s). You may have a shopping cart and process

payment transactions yourself or use a third-party

service.■ If your site doesn't support transactions but your

customers call, complete and submit a form or email you to make a purchase order, booking, etc.–Advertising programs, or

–Other types of traffic programs.

Enter the percentage of income generated from the Internet. If you do

not know the exact percentage, provide an

estimate.

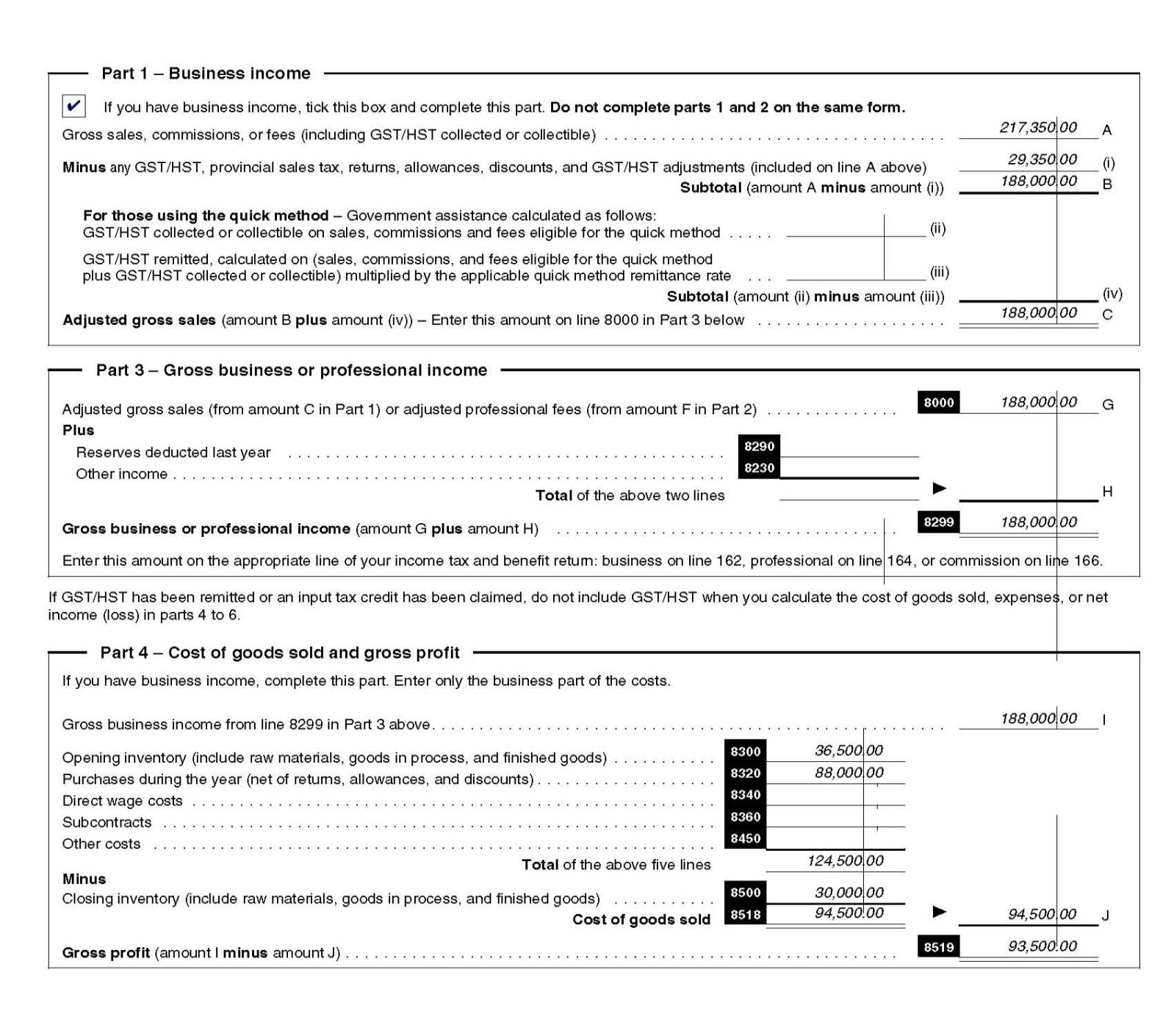

Part 1 – Business income

On line A enter the gross sales, commissions, or fees (including GST/HST, collected or collectible).

On line (i) enter any GST/HST, provincial sales tax, returns, allowances, discounts and GST/HST adjustments (included on line A). Line B is the total of line A minus line (i).

For more information on the quick method and examples of how it works, see Guide RC4058, Quick Method of Accounting for GST/HST.

Line C (Adjusted gross sales) is the total of the amounts from line B plus line (iv).

As mentioned in Chapter 1 on page 6, professional

activities are business activities. Usually, you calculate your income from professional activities using the same rules as for a business. However, some aspects of professional

activities are different from those of other types of

businesses. Some of these differences are discussed in this section.Professional fees

plus:

■all amounts receivable at the end of the current year for professional services you provided during the current year; and

On line D enter the gross professional fees including WIP and GST/HST collected or collectible.

On line (i) enter any GST/HST, provincial sales tax, returns, allowances, discounts and GST/HST adjustments (included on line D) and any WIP at the end of the year you elected to exclude. Line E is the total of line D minus line (i).

■The subtotal at line (iv) is line (ii) minus line (iii).

For more information about the Quick method and examples of how it works, see Guide RC4058, Quick Method of Accounting (or GST/HST.

■a dentist;

■a lawyer (including a notary in Quebec);

You can also exclude your WIP by doing the following:

■On the “WIP, end of the year, per election to exclude WIP” line, write the amount you included as WIP at the end of the year in your professional fees on line D.

Part 3 – Gross business or professional income

Line 8000 – Adjusted gross sales or adjusted professional fees

Line 8230 – Other income

Enter the total income you received from other sources. Some examples of other income you would report on this line are:

If you used the quick method to calculate your GST/HST remittances, report the 1% credit (maximum $300) that you claimed on line 107 of your GST/HST return. For more information, see Interpretation Bulletin IT-273, Government Assistance – General Comments.

Note

Report the amount received in the year for the GST/HST rebate for partners that relates to eligible expenses other than CCA on line 9974 in Part 6 on page 3 of

Form T2125. See “Part 6 – Your net income (loss)” on page 30.

If the rebate, grant, or assistance is for a depreciable asset, subtract the amount you received from the asset’s capital cost.

This will affect the amount of CCA you can claim for that asset. For

information about CCA, see Chapter 4 beginning on page 32. If the asset

qualifies for the investment tax credit, this reduction to the capital

cost will also affect your claim for the investment tax credit. For more

information, see

Form T2038 (IND), Investment Tax Credit (Individuals).

Complete this part if you have a business and your business buys goods for resale or makes goods for sale.

Claim the cost of the goods you buy or make for sale in the fiscal

period in which you sell them. Enter only the

business part of the costs on the form.

Line 8300 – Opening inventory and Line 8500 – Closing inventory

Enter your opening and closing inventory on the

appropriate lines. These amounts must include raw

materials, goods in process, and finished goods. The way you value your

inventory is important in determining your income. For income tax

purposes, choose one of the

following two methods:

If this is your first year of reporting business income, you can choose either method to value your inventory. In your first year of business, you will not have an opening

inventory amount to enter on line 8300. If this is not your first year of business, continue to use the same method you used in past years. The value of your inventory at the start of a fiscal period has to be the same as the value of your inventory at the end of the preceding fiscal period.Do an actual stock count at the end of each fiscal period, unless you use a perpetual inventory system. Under this system, you do periodic stock counts and keep a written record of each count. Remember to keep your inventory records with your other records.

For more information, see Interpretation

Bulletin IT-504R2-CONSOLID, Visual Artists and Writers.Gifts of inventory by an artist

If you donate a work of art you created, you may not have to report a profit on your donation for income tax purposes. To benefit from this tax treatment, your gift must fall under the definition of gifts of certified cultural property. For more information about gifts and donations, see

Pamphlet P113, Gifts and Income Tax.

Line 8340 – Direct wage costs

Include the remuneration you paid to employees who work directly in the

manufacture of your goods. Do not include:

Line 8360 – Subcontracts

Enter all the costs of hiring outside help to perform tasks related to the goods you sell.

Enter your gross profit, which is your gross business income (line 8299 in Part 3 on page 2) minus your cost of goods sold (line 8518).

The following example summarizes this chapter. Since the rules for calculating business and professional income are similar, our example focuses on a business.

Cathy completes “Part 1 – Business income,” “Part 3 – Gross business or professional income,” and “Part 4 – Cost of goods sold and gross profit” on Form T2125 as follows:

|

|---|

www.cra.gc.ca 19

“Enter only the business part” means that you do not include any of the following in your expenses:

■most life insurance premiums (for more information, see “Line 8690 – Insurance” on page 21);

■the part of expenses that can be attributed to the non-business use of business property; and

For more information, see Interpretation Bulletin IT-417, Prepaid Expenses and Deferred Charges.

Part 5 – Net income (loss) before adjustments

You cannot deduct expenses for advertising directed mainly at a Canadian market when you advertise with a foreign broadcaster.

Line 8523 – Meals and entertainment

However, special rules can affect your claim for meals in these cases. For more information, see “Line 9200 – Travel” on page 23 and “Convention expenses” on page 27.

These limits do not apply if:

■the meal and entertainment expenses you incur are for a fund-raising event that was mainly for the benefit of a registered charity; or

■you provide meals to an employee housed at a

temporary work camp constructed or installed

specifically to provide meals and accommodation to employees working at a construction site (note that the employee cannot be expected to return home daily).Self-employed foot and bicycle couriers and rickshaw drivers can deduct the cost of extra food and beverages they must consume in a normal working day (8 hours) because of the nature of their work. The daily flat rate that can be claimed is $17.50.

If you are claiming this deduction you should be prepared to provide log books showing the days worked and the hours worked on each of these days during the tax year.