Record the information store ledger card using fifo

Unit Competency Outcome

|

|

| Name : Signature : |

|---|

|

|

|

|

here………………………………………………………………………………………………….......................................................... .................

|

||

|---|---|---|

|

|

|

The student will demonstrate skills and knowledge required to comply with organisational inventory procedures, reconcile inventory records to general ledgers, record inventory flows, prepare schedules and produce ad hoc reports.

Assessment description

Submission

You must submit:

a. Cost of inventories

b. Inventories

c. Net realisable value

d. Replacement costs

e. Non-current assets

|

|

|

|

Page 4 of 22

insignificant cost.

Question 3

Question 4

4 Sold goods for cash $690 plus GST (cost of goods sold $345)

6 Purchased inventory on credit from Lang $3,200 plus GST

returned $450)

22 Anderson withdrew inventory for personal use $231 including GST.

Unit Competency Outcome V2.0 Dec 2019

Page 6 of 22

|

|

|

|---|---|---|

|

|

|

|

|

(e) Prepare the general journal entry to record closing stock into the ledger using average cost.

(f) Prepare the trading statement where the FIFO method is used.

A firm uses a perpetual inventory system. Details of an item of inventory disclosed:

|

|

|---|

a print out of the following:

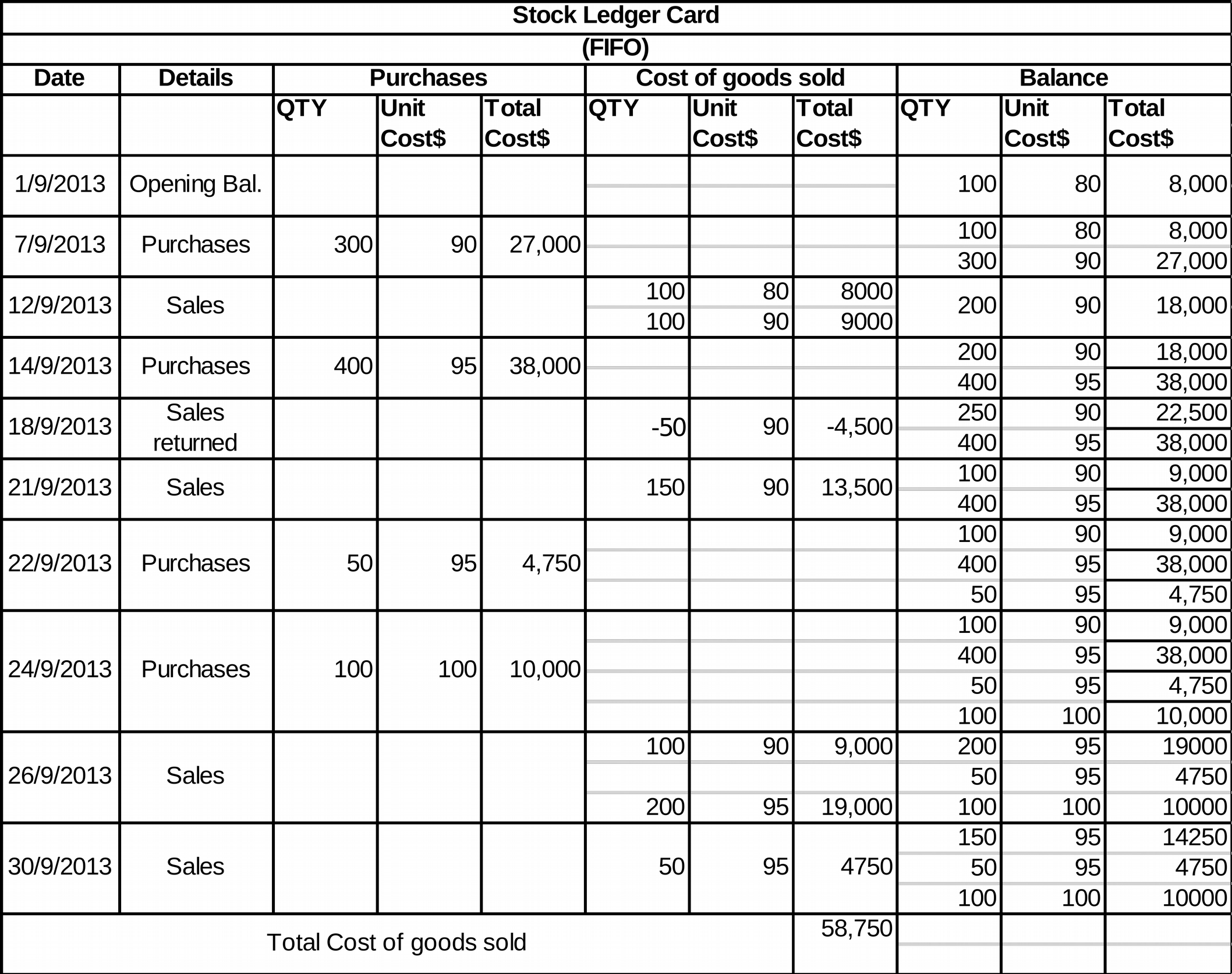

a. Store Ledger Card

Question 7

Assume the following data for a retail business in 2013: Net sales: $640,000

Gross profit: 224,000

Expenses: 64,000

Net profit after tax: 160,000

Ending inventory: 94,000

Beginning inventory: 86,000Question 8

A firm has these inventory records for January 2013.

(a) Prepare the January profit and loss statement, showing for FIFO, LIFO and weighted-average cost. Show your calculation and use the periodic inventory system to calculate cost of goods sold.

| Weighted-average | |||

|---|---|---|---|

|

|||

|

|||

|

|||

|

|||

c. Report net profit between the extremes of FIFO and LIFO? d. Report inventory on the balance sheet at the most current cost?

Unit Competency Outcome V2.0 Dec 2019

Your assessor will be looking for Evidence of the ability to

describe the key steps in the inventory management processes and relevant documentation and recording systems

|

|---|

Unit Competency Outcome V2.0 Dec 2019 Page 15 of 22

Perpetual inventory system is a system of inventory accounting in which real time tracking of inventory movements is done.

2. Status of accounts updation

In periodic inventory system, inventory accounts do not reflect accurate picture at all times. The correct inventory position is only updated in accounts at the time of physical counting.In perpetual inventory system, cost of goods sold can be determined at any time on the basis of real time records maintained in the system.

5. Cost involved

Periodic inventory system is simpler and involves lower cost.

7. Preferred by

Periodic inventory system is preferred by smaller enterprises with lower sales volume and where physical counting of inventory is more feasible.(a)

General journal of Anderson

| Date | |||

|---|---|---|---|

| June 1 | 40000 | 40000 | |

|

|

5500 | |

| 4 | 759 | ||

| 345 | 345 | ||

| 6 |

|

3520 | |

| 9 |

|

7590 | |

| 3450 | 3450 | ||

| 12 | 220 | ||

| 15 |

|

2970 |

|

| 1350 | 1350 | ||

| 19 | 990 | ||

| 450 | 450 |

Unit Competency Outcome V2.0 Dec 2019 Page 17 of 22

| 1/7 Balance b/d 9390 | |

|---|---|

| Cost of goods sold | |

|

|

Question 5

Sales 80,500

Less COGS 63,500

Gross profit 17,000

Opening inventory 8,000 (8800-8800/ (1+10%)) Purchases 79,750

Goods available for sale 87,750

Less Closing Stock 24,250

Per unit = 92.37

Therefore, closing inventory = per unit*quantity=92.37*250 = $23092.50

|

|---|

Unit Competency Outcome V2.0 Dec 2019

Page 20 of 22