Posting procedure step including chart accounts

Isabela State University-CBAPA 1

Introduction

The module, Recording Business Transaction, contains materials and activities related to explaining the sequential steps in the accounting cycle, analyzing business transactions and preparing the journal entries, developing a chart of accounts, posting procedures and preparing the trial balance.

4. Outline the steps in analyzing transactions and state the role of source documents.

5. Analyze the impact of transactions on the elements and the specific accounts. 6. Apply the rules of debits and credits in analyzing business transactions.

11. Develop chart of accounts.

12. Prepare and explain the use of a trial balance.

Department of Accountancy & Management Accounting

Accty 111- FINANCIAL ACCOUNTING & REPORTING

General management: Imagine running Ford Motors, Philippine General Hospital, University of Santo Tomas, a McDonalds franchise, a Trek bike shop. All general managers need to understand where the enterprise’s cash comes from and where it goes in order to make wise business decisions.

Marketing: A marketing specialist at a company like Procter & Gamble develops strategies to help the sales force be successful. But making a sale is meaningless unless it is a profitable sale. Marketing people must be sensitive to costs and benefits, which accounting helps them quantify and understand.

Isabela State University-CBAPA 3

The steps in the cycle and their aims follow:

During the Accounting Period

STEP 1 Identification of Events to be Recorded

AIM: To gather information about transactions or events generally

through the source documents.

STEP 7 Adjusting Journal Entries are Journalized and

Posted

AIM: To record the accruals, expiration of deferrals, estimations and

other events from the worksheet.

STEP 8 Closing Journal Entries are Journalized and

Posted

AIM: To close temporary accounts and transfer profit to owner’s

equity.

SOURCE DOCUMENTS

Source documents identify and describe transactions and

events entering the accounting system. They can be in hard copy or

electronic form. Examples are sales receipts, checks, purchase orders,

bills from suppliers, payroll records, and bank

Dr.jeanettegonzales.cpa

statements. For example, cash registers record each sale on a tape or electronic file. This record is a source document for recording sales in the accounting system. Source documents are objective and reliable evidence about transactions and events and their amounts.

Transactions and events are the starting points in the accounting cycle. By relying on source documents, transactions and events can be analyzed as to how they will affect performance and financial position. Source documents identify and describe transactions and events entering the accounting process. These original written evidences contain information about the nature and the amounts of the transactions. These are the bases for the journal entries; some of the more common source documents are sales invoices, cash register tapes, official receipts, bank deposit slips, bank statements, checks, purchase orders, time cards and statements of account. Specimens and discussions on some of these documents will in Module 7.

Application of Double-Entry: T accounts show how the transaction affects the accounting equation. Note that this is not part of the accounting records but is undertaken before recording a transaction in order to understand the effects of the transaction.

Journal Entry: A journal entry is a notation that records a single transaction in the chronological accounting record known as a journal (sometimes called the book of original entry because it is where transactions first enter the accounting records).

3. Determine whether each account is increased or decreased by the transaction. 4. Using the rules of debit and credit, determine whether to debit or credit the account to record its increase or decrease.

Dr.jeanettegonzales.cpa

Transactions (business transactions) are a business’s economic events recorded by accountants. Transactions may be external or internal.

External transactions involve economic events between the company and some outside enterprise. For example, Campus Pizza’s purchase of cooking equipment from a supplier, payment of monthly rent to the landlord, and sale of pizzas to customers are external transactions.

| EXAMPLE: |

|---|

TRANSACTION: On August 1, Lanz Red invests P400,000 in cash to form

Red Design Studio. ANALYSIS: The journal entry to record an owner’s

investment in the business

INCREASES asset account CASH with a debit

INCREASES the owner’s equity account L. Red, capital with a

credit

(apply the rules of debit and credit)

APPLICATION OF DOUBLE ENTRY |

|

|

|---|

as the appropriate asset account (for example, Equipment).

Lesson 3Business Transactions are Journalized (STEP 2)

Isabela State University-CBAPA 6

Department of Accountancy & Management Accounting

3. It helps to prevent or locate errors because the debit and credit amounts for each entry can be easily compared.

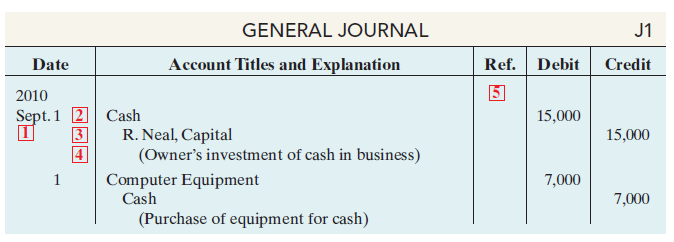

JOURNALIZING

Entering transaction data in the journal is known as

journalizing. Companies make separate journal entries

for each transaction. A complete entry consists of: (1) the date of the

transaction, (2) the accounts and amounts to be debited and credited,

and (3) a brief explanation of the transaction.

5. Credit. The credit amount for each account is entered in this column.

Dr.jeanettegonzales.cpa

Assume that Maria Concepcion Jennifer Perez-Manalo established her own wedding consultancy with an initial investment of P250.000 on May 1.

The journal entry is shown below:

Isabela State University-CBAPA 8

2 The debit account title (that is, the account to be debited) is entered first at the extreme left margin of the column headed “Account Titles and Explanation,” and the amount of the debit is recorded in the Debit column.

3 The credit account title (that is, the account to be credited) is indented and entered on the next line in the column headed “Account Titles and Explanation,” and the amount of the credit is recorded in the Credit column.

After the transaction or event has been identified and measured, it is recorded in the journal. The process of recording a transaction is called journalizing. The following are the transactions for Wedding Planner during the month of May. The double-entry system will be used.

To understand the nature of the affected accounts, the letter A (for asset), L (liability) or OE (owner's equity) is inserted after each entry. In addition, owner's equity is further classified into OE:I (income) and OE:E (expenses).

Isabela State University-CBAPA 9

Rules Increases in assets are recorded by debits. Increases in owner's equity are recorded by credits.

Entry Increase in assets is recorded by a debit to cash. Increase in owner's equity is recorded by a credit to Cruz, Capital.

Entry Increase in assets is recorded by a debit to prepaid rent. Decrease in assets is recorded by a credit to cash.

Dr. Cr.

Dr. Cr.

Cash (A) 210,000

Notes Payable (L) 210,000

___________________________________________________________________

Department of Accountancy & Management Accounting

Accty 111- FINANCIAL ACCOUNTING & REPORTING

Dr. Cr.

Service Vehicle (A) 420,000

Cash (A ) 420,000

___________________________________________________________________

Insurance Premiums Paid (Exchange of Assets)

May 4 Paid Prudential Guarantee and Assurance, Inc. P14,400 for a

one-year comprehensive insurance coverage on the service vehicle.

Prepaid Insurance (A) 14,400

Cash (A) 14,400

___________________________________________________________________

Office Equipment Acquired on Account (Exchange and Source of

Assets)

May 5 Acquired office equipment from Fair and Square Emporium for

P60,000; paying P15,000 in cash and the balance next month. Note: A

compound entry is needed for this transaction.

Analysis Assets increased. Assets decreased. Liabilities increased.

Office Equipment (A) 60,000

Cash (A) 15,000

Accounts Payable (L) 45,000

___________________________________________________________________

Supplies Purchased on Account (Source of Assets)

May 8 Purchased supplies on credit for P18,000from San

Jose Merchandising.

Analysis Assets increased. Liabilities increased.

Department of Accountancy & Management Accounting

Accty 111- FINANCIAL ACCOUNTING & REPORTING

Analysis Assets decreased. Liabilities decreased.

Rules Decreases in assets are recorded by credits. Decreases in liabilities are recorded by debits.

Rules Increases in assets are recorded by debits. Increases in owner's equity are recorded by credits.

Entry Increase in assets is recorded by a debit to cash. Increase in owner's equity is recorded by a credit to consulting revenues.

Entry Decrease in owner's equity is recorded by a debit to salaries expense. Decrease in assets is recorded by a credit to cash.

Dr. Cr. .

Department of Accountancy & Management Accounting

Accty 111- FINANCIAL ACCOUNTING & REPORTING

Dr. Cr.

Cash (A) 10,000

Unearned Referral Revenues (L) 10,000

___________________________________________________________________

Revenues Earned on Account (Source of Assets)

May 19 Coordinated and finalized elaborate bridal arrangements for three

couples and billed fees of P12,000 per couple. Additional services

include documents preparation, consultation with a feng shui expert as

to the ideal wedding date for prosperity and harmony, provision for

limousine service and honeymoon trip.

Accounts Receivable (A) 36,000

Consulting Revenues (OE:I) 36,000

___________________________________________________________________

Withdrawal of Cash by Owner (Use of Assets)

May 25 Cruz withdrew P14,000 for personal expenses.

Analysis Assets decreased. Owner's equity decreased.

Analysis Assets decreased. Owner's equity decreased.

Dr.jeanettegonzales.cpa

Rules Decreases in assets are recorded by credits. Decreases in owner's equity are recorded by debits.

Entry Decrease in owner's equity is recorded by a debit to salaries expense. Decrease in assets is recorded by a credit to cash.

Entry Decrease in owner's equity is recorded by a debit to utilities expense. Increase in liabilities is recorded by a credit to utilities payable.

Dr. Cr.

Cash (A) 24,000

Accounts Receivable (A) 24,000

___________________________________________________________________

Expenses Incurred and Paid (Use of Assets)

May 31 Settled the electricity bill of P3,000 for the month.

Analysis Assets decreased. Owner's equity decreased.

Dr.jeanettegonzales.cpa

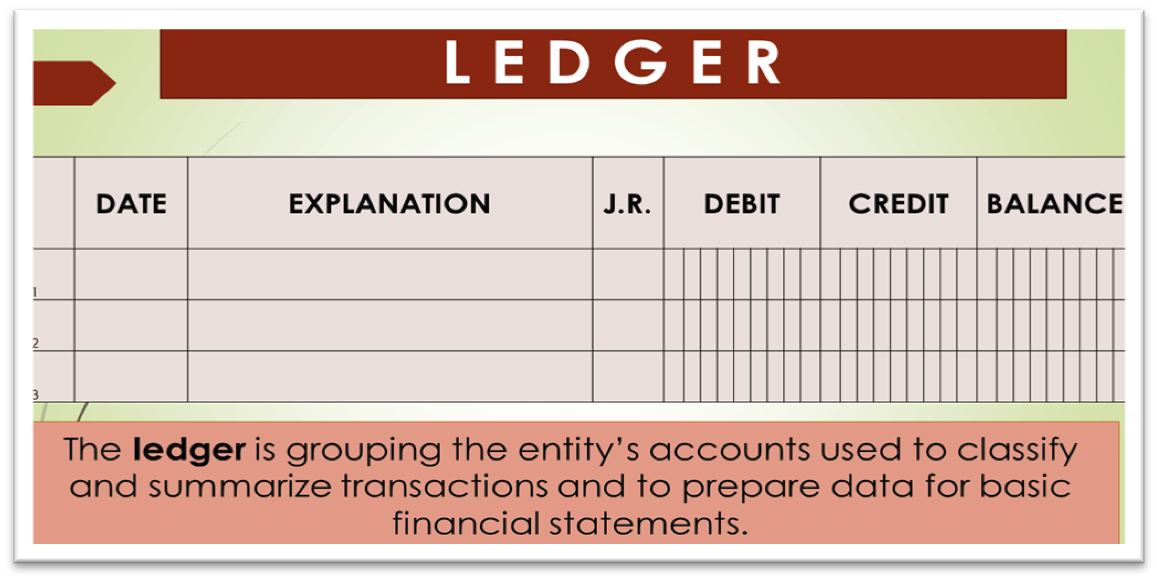

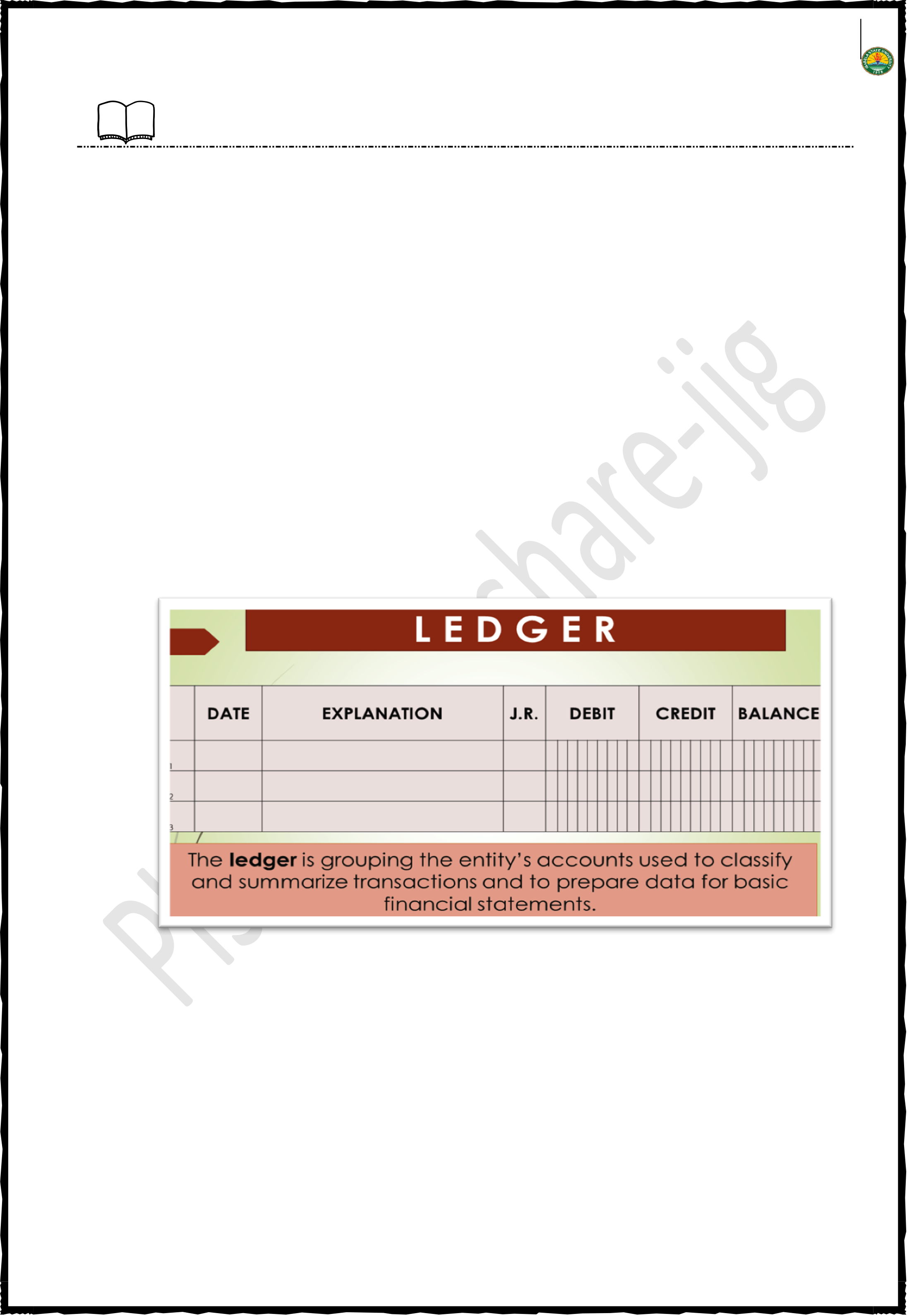

THE LEDGER-Book of Final Entry

The entire group of accounts maintained by a company is the ledger. The ledger keeps in one place all the information about changes in specific account balances. Although some firms may use various ledgers to accumulate certain detailed information, all firms have a general ledger. A general ledger is the "reference book" of the accounting system and is used to classify and summarize transactions, and to prepare data for basic financial statements.. A general ledger contains all the asset, liability, and owner’s equity accounts. Whenever we use the term “ledger” in this module, we are referring to the general ledger, unless we specify otherwise.

ACCOUNTING

Each account has its own record in the ledger. Every account in the

ledger maintains the basic format of the T-account but offers more

information (e.g. the account number

Dr.jeanettegonzales.cpa

at the upper right corner and the journal reference column). Compared to a journal, a ledger organizes information by account.

CHART OF ACCOUNTS

POSTING (Step 3)

Wedding Planner

420 Referral Revenues

Expenses

550 Utilities Expense

560 Depreciation Expense-

590 Interest Expense

Posting means transferring the amounts from the journal to the appropriate accounts in the ledger. Debits in the journal are posted as debits in the ledger, and credits in the journal as credits in the ledger.

Accty 111- FINANCIAL ACCOUNTING & REPORTING

The steps are illustrated as follows:

1. Transfer the date of the transaction from the journal to the

ledger.

At the end of an accounting period, the debit or credit balance of each account must be determined to enable us to come up with a trial balance.

a. Each account balance is determined by footing (adding) all the debits and credits.

Isabela State University-CBAPA 17

Department of Accountancy & Management Accounting

| May 1 8,000 4 420,000 4 14,400 5 15,000 9 10,000 13 6,600 25 14,000 27 7,200 31 3,000 498,200 |

|

|

|

|---|---|---|---|

Office Equipment

May 5 60,000

Balance 60,000

Liabilities

Owner’s Equity

Cruz, Capital

May 1 250,000

Balance 250,000Cruz, Withdrawals

May 25 14,000

Balance 14,000

Accty 111- FINANCIAL ACCOUNTING & REPORTING

|

|---|

The Recording Process Illustrated

Study the transaction analyses carefully. The purpose of transaction analysis is first to identify the type of account involved, and then to determine whether to make a debit or a credit to the account. You should always perform this type of analysis before preparing a journal entry.

Accty 111- FINANCIAL ACCOUNTING & REPORTING

Lesson 5Trial Balance Preparation (Step 4)

left column and credit balances in the right column. The trial balance is a list of all

accounts with their respective debit or credit balances. The primary purpose of a trial

preparing financial statements.

The procedures in the preparation of a trial balance follow:

4. Compare the totals.

The trial balance is a control device that helps minimize accounting errors. When the

overstated.

The trial balance for the illustration follows:

Accounts Receivable 12,000

Supplies 18,000

Notes Payable P210,000

Accounts Payable 53,000

Consulting Revenues 62,400

Salaries Expense 13,800

Isabela State University-CBAPA 20

balance would bring this error to light.

Lesson 6Locating Errors

LOCATING ERRORS

An inequality in the totals of the debits and credits would

automatically signal the presence of an error. These errors

include:

1. Error in posting a transaction to the ledger:

• a balance was entered in the wrong balance column.

3. Error in preparing the trial balance:

2. If the error does not lie in addition, determine the exact amount by which the trial balance is out of balance. The amount of the discrepancy is often a clue to the source of the error. If the discrepancy is divisible by 9, this suggests either a transposition (reversing the order of numbers) error or a slide (moving of the decimal point). For example, assume that the cash account

Dr.jeanettegonzales.cpa