Marks find the yield maturity the companys debt

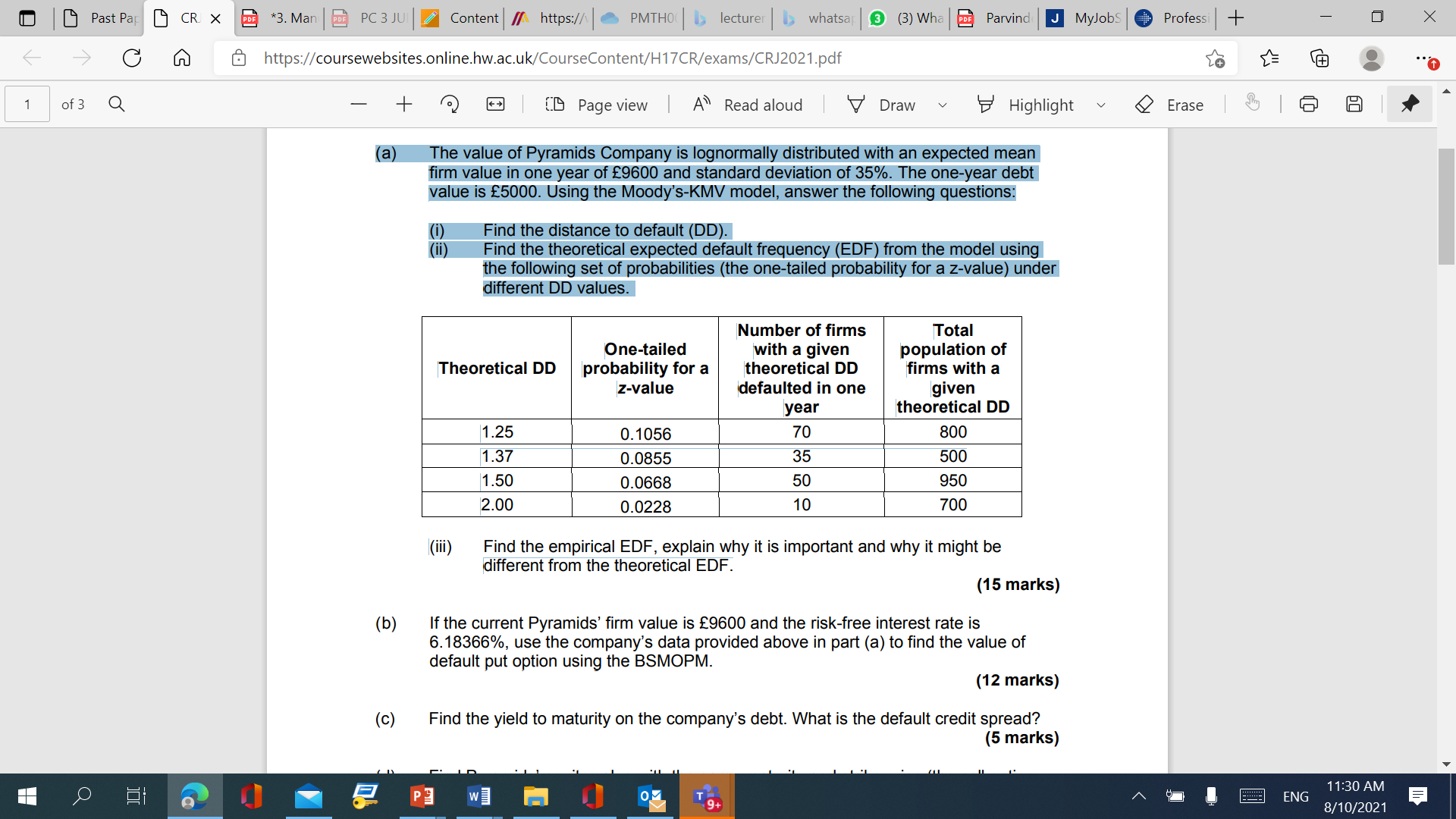

(ii) Find the theoretical expected default frequency (EDF) from the model using the following set of probabilities (the one-tailed probability for a z-value) under different DD values.

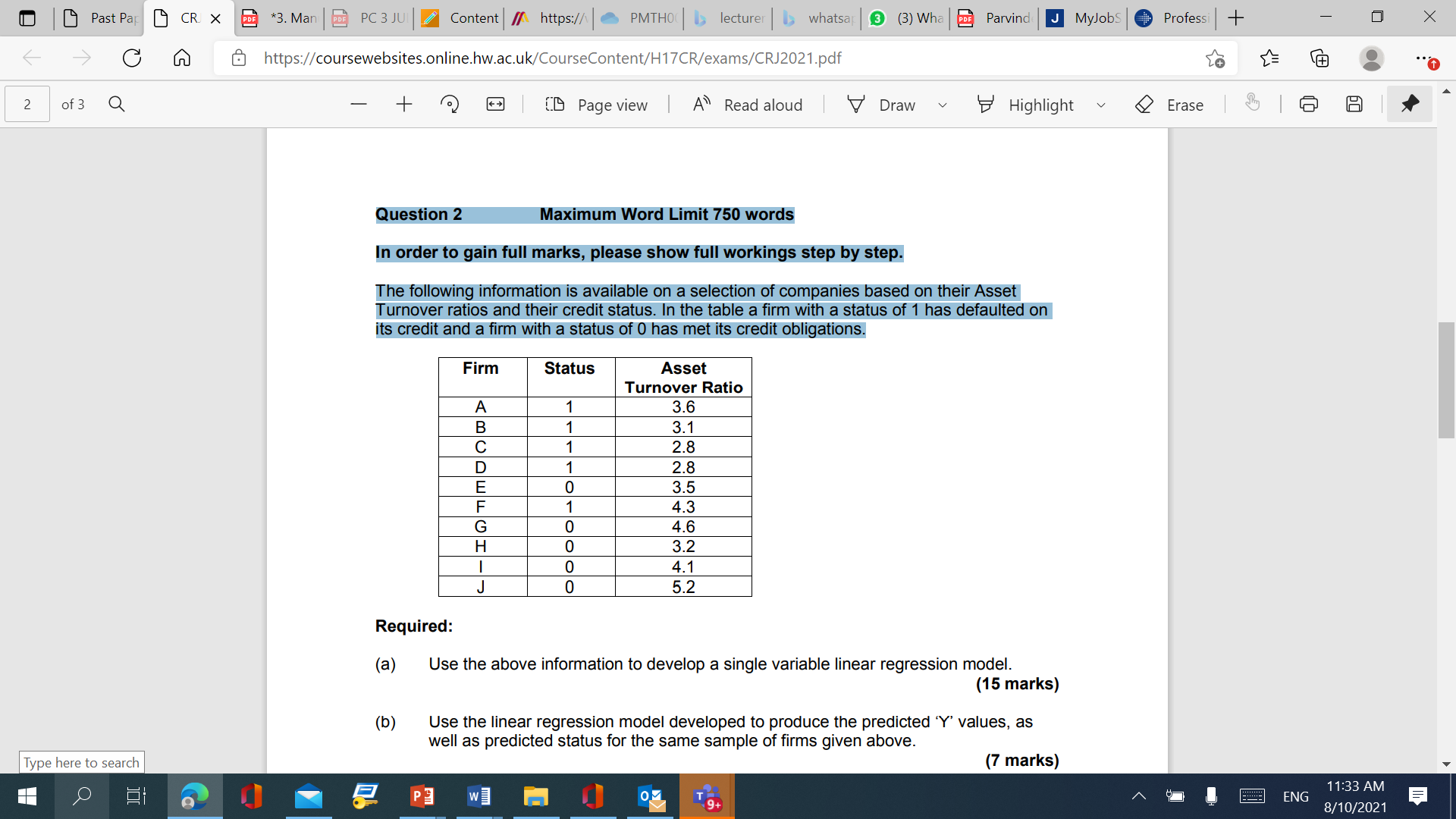

In order to gain full marks, please show full workings step by step. The following information is available on a selection of companies based on their Asset Turnover ratios and their credit status. In the table a firm with a status of 1 has defaulted on its credit and a firm with a status of 0 has met its credit obligations.

(d) A bond issue of a company matures in one year. The coupon rate is 9% and the bond price in the market is £101.20. A government bond of a one-year maturity with same coupon rate (9%) trades in the market at £104.81. If the risk-free rate is 4%, what is the default probability of the company’s bond given a recovery rate of 65%? (8 marks)

Question 3

(d) Describe three different methods of monitoring outstanding receivables. (5 marks