Googles founders and management control the company

Page 2 of 21

CHAPTER 15

In discussing common stock features, we focus on shareholder rights and dividend payments. For preferred stock, we explain what the “preferred” means, and we also debate whether preferred stock is really debt or equity.

Common Stock Features

Directors are elected at an annual shareholders’ meeting by a vote of the holders of a majority of shares who are present and entitled to vote. However, the exact mechanism for electing directors differs across companies. The most important difference is whether shares must be voted cumulatively or voted straight.

file:///C:/Users/dehartjr/Calibre%20Library/Ross,%20Stephen%20A_/Corporate%20Finan... 5/21/2012

Will Smith get a seat on the board? If we ignore the possibility of a five-way tie, then the answer is yes. Smith will cast 20 × 4 = 80 votes, and Jones will cast 80 × 4 = 320 votes. If Smith gives all his votes to himself, he is assured of a directorship. The reason is that Jones can’t divide 320 votes among four candidates in such a way as to give all of them more than 80 votes, so Smith will finish fourth at worst.

In general, if there are N directors up for election, then 1/(N + 1) percent of the stock plus one share will guarantee you a seat. In our current example, this is 1/(4 + 1) = 20 percent. So the more seats that are up for election at one time, the easier (and cheaper) it is to win one.

As we’ve illustrated, straight voting can “freeze out” minority shareholders; that is the reason many states have mandatory cumulative voting. In states where cumulative voting is mandatory, devices have been worked out to minimize its impact.

One such device is to stagger the voting for the board of directors. With staggered elections, only a fraction of the directorships are up for election at a particular time. Thus, if only two directors are up for election at any one time, it will take 1/(2 + 1) = 33.33 percent of the stock plus one share to guarantee a seat.

2. Staggering makes takeover attempts less likely to be successful because it makes it more difficult to vote in a majority of new directors.

We should note that staggering may serve a beneficial purpose. It provides “institutional memory,” that is, continuity on the board of directors. This may be important for corporations with significant long-range plans and projects.

Classes of Stock

Some firms have more than one class of common stock. Often, the classes are created with unequal voting rights. The Ford Motor Company, for example, has Class B common stock, which is not publicly traded (it is held by Ford family interests and trusts). This class has 40 percent of the voting power, even though it represents less than 10 percent of the total number of shares outstanding.

file:///C:/Users/dehartjr/Calibre%20Library/Ross,%20Stephen%20A_/Corporate%20Finan... 5/21/2012

Page 5 of 21

2. The right to share proportionally in assets remaining after liabilities have been paid in a liquidation.

3. The right to vote on stockholder matters of great importance, such as a merger. Voting is usually done at the annual meeting or a special meeting.

Some important characteristics of dividends include the following:

1. Unless a dividend is declared by the board of directors of a corporation, it is not a liability of the corporation. A corporation cannot default on an undeclared dividend. As a consequence, corporations cannot become bankrupt because of nonpayment of dividends. The amount of the dividend and even whether it is paid are decisions based on the business judgment of the board of directors.

file:///C:/Users/dehartjr/Calibre%20Library/Ross,%20Stephen%20A_/Corporate%20Finan... 5/21/2012

Page 6 of 21

A preferred dividend is not like interest on a bond. The board of directors may decide not to pay the dividends on preferred shares, and their decision may have nothing to do with the current net income of the corporation.

Dividends payable on preferred stock are either cumulative or noncumulative; most are cumulative. If preferred dividends are cumulative and are not paid in a particular year, they will be carried forward as an arrearage. Usually, both the accumulated (past) preferred dividends and the current preferred dividends must be paid before the common shareholders can receive anything.

In the 1990s, firms began to sell securities that looked a lot like preferred stock but were treated as debt for tax purposes. The new securities were given interesting acronyms like TOPrS (trust-originated preferred securities, or toppers), MIPS (monthly income preferred securities), and QUIPS (quarterly income preferred securities), among others. Because of various specific features, these instruments can be counted as debt for tax purposes, making the interest payments tax deductible. Payments made to investors in these instruments are treated as interest for personal income taxes for individuals. Until 2003, interest payments and dividends were taxed at the same marginal tax rate. When the tax rate on dividend payments was reduced, these instruments were not included, so individuals must still pay their higher income tax rate on dividend payments received from these instruments.

15.2 Corporate Long-Term Debt

From a financial point of view, the main differences between debt and equity are the following:

1. Debt is not an ownership interest in the firm. Creditors generally do not have voting power.

Sometimes it is not clear if a particular security is debt or equity. For example, suppose a corporation issues a perpetual bond with interest payable solely from corporate income if, and only if, earned. Whether or not this is really a debt is hard to say and is primarily a legal and semantic issue. Courts and taxing authorities would have the final say.

Corporations are very adept at creating exotic, hybrid securities that have many features of equity but are treated as debt. Obviously, the distinction between debt and equity is very important for tax purposes. So, one reason that corporations try to create a debt security that is really equity is to obtain the tax benefits of debt and the bankruptcy benefits of equity.

file:///C:/Users/dehartjr/Calibre%20Library/Ross,%20Stephen%20A_/Corporate%20Finan... 5/21/2012

Page 8 of 21

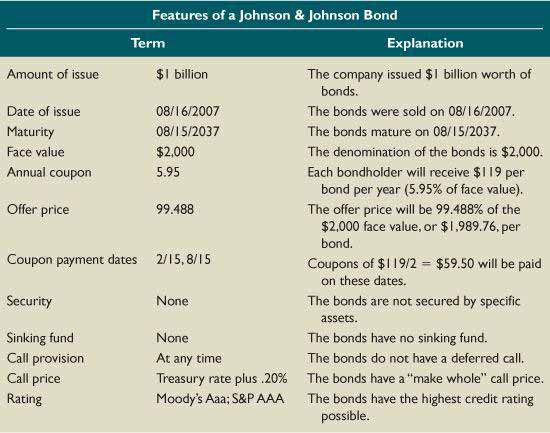

There are many other dimensions to long-term debt, including such things as security, call features, sinking funds, ratings, and protective covenants. The following table illustrates these features for a bond issued by Johnson & Johnson. If some of these terms are unfamiliar, have no fear. We will discuss them all presently.

The Indenture

The indenture is the written agreement between the corporation (the borrower) and its creditors. It is sometimes referred to as the deed of trust.6 Usually, a trustee (a bank perhaps) is appointed by the corporation to represent the bondholders. The trust company must (1) make sure the terms of the indenture are obeyed, (2) manage the sinking fund (described in the following pages), and (3) represent the bondholders in default, that is, if the company defaults on its payments to them.

4. The repayment arrangements.

5. The call provisions.

Terms of a Bond

file:///C:/Users/dehartjr/Calibre%20Library/Ross,%20Stephen%20A_/Corporate%20Finan... 5/21/2012

This means that the company has a registrar who will record the ownership of each bond and record any changes in ownership. The company will pay the interest and principal by check mailed directly to the address of the owner of record. A corporate bond may be registered and have attached “coupons.” To obtain an interest payment, the owner must separate a coupon from the bond certificate and send it to the company registrar (the paying agent).

Alternatively, the bond could be in bearer form. This means that the certificate is the basic evidence of ownership, and the corporation will “pay the bearer.” Ownership is not otherwise recorded, and, as with a registered bond with attached coupons, the holder of the bond certificate detaches the coupons and sends them to the company to receive payment.

Mortgage securities are secured by a mortgage on the real property of the borrower. The property involved is usually real estate, for example, land or buildings. The legal document that describes the mortgage is called a mortgage trust indenture or trust deed.

Sometimes mortgages are on specific property, for example, a railroad car. More often, blanket mortgages are used. A blanket mortgage pledges all the real property owned by the company.7

At the current time, public bonds issued in the United States by industrial and financial companies are typically debentures. However, most utility and railroad bonds are secured by a pledge of assets.

Seniority

Bonds can be repaid at maturity, at which time the bondholder will receive the stated, or face, value of the bond, or they may be repaid in part or in entirety before maturity. Early repayment in some form is more typical and is often handled through a sinking fund.

A sinking fund is an account managed by the bond trustee for the purpose of repaying the bonds. The company makes annual payments to the trustee, who then uses the funds to retire a portion of the debt. The trustee does this by either buying up some of the bonds in the market or calling in a fraction of the outstanding bonds. This second option is discussed in the next section.

The Call Provision

A call provision allows the company to repurchase, or “call,” part or all of the bond issue at stated prices over a specific period. Corporate bonds are usually callable.

In just the last few years, a new type of call provision, a “make-whole” call, has become very widespread in the corporate bond market. With such a feature, bondholders receive approximately what the bonds are worth if they are called. Because bondholders don’t suffer a loss in the event of a call, they are “made whole.”

To determine the make-whole call price, we calculate the present value of the remaining interest and principal payments at a rate specified in the indenture. For example, looking at our Johnson & Johnson issue, we see that the discount rate is “Treasury rate plus .20%.” What this means is that we determine the discount rate by first finding a U.S. Treasury issue with the same maturity. We calculate the yield to maturity on the Treasury issue and then add on an additional .20 percent to get the discount rate we use.

A positive covenant is a “thou shalt” type of covenant. It specifies an action that the company agrees to take or a condition the company must abide by. For example, the company must maintain its working capital at or above some specified minimum level.

Want detailed information on the amount and terms of the debt issued by a particular firm? Check out its latest financial statements by searching SEC filings at www.sec.gov.

Credit ratings are important because defaults really do occur, and, when they do, investors can lose heavily. For example, in 2000, AmeriServe Food Distribution, Inc., which supplied restaurants such as Burger King with everything from burgers to giveaway toys, defaulted on $200 million in junk bonds. After the default, the bonds traded at just 18 cents on the dollar, leaving investors with a loss of more than $160 million.

Even worse in AmeriServe’s case, the bonds had been issued only four months earlier, thereby making AmeriServe an NCAA champion. While that might be a good thing for a college basketball team such as the University of Kentucky Wildcats, in the bond market NCAA means “No Coupon At All,” and it’s not a good thing for investors.

With floating-rate bonds (floaters), the coupon payments are adjustable. The adjustments are tied to an interest rate index such as the Treasury bill interest rate or the 30-year Treasury bond rate.

The value of a floating-rate bond depends on exactly how the coupon payment adjustments are defined. In most cases, the coupon adjusts with a lag to some base rate. For example, suppose a coupon rate adjustment is made on June 1. The adjustment might be based on the simple average of Treasury bond yields during the previous three months. In addition, the majority of floaters have the following features:

Bond features are really only limited by the imaginations of the parties involved. Unfortunately, there are far too many variations for us to cover in detail here. We therefore close out this section by mentioning only a few of the more common types.

Income bonds are similar to conventional bonds, except that coupon payments are dependent on

A put bond allows the holder to force the issuer to buy the bond back at a stated price. For example, International Paper Co. has bonds outstanding that allow the holder to force International Paper to buy the bonds back at 100 percent of face value given that certain “risk” events happen. One such event is a change in credit rating from investment grade to lower than investment grade by Moody’s or S&P. The put feature is therefore just the reverse of the call provision.

A given bond may have many unusual features. Two of the most recent exotic bonds are CoCo bonds, which have a coupon payment, and NoNo bonds, which are zero coupon bonds. CoCo and NoNo bonds are contingent convertible, putable, callable, subordinated bonds. The contingent convertible clause is similar to the normal conversion feature, except the contingent feature must be met. For example, a contingent feature may require that the company’s stock trade at 110 percent of the conversion price for 20 out of the most recent 30 days. Valuing a bond of this sort can be quite complex, and the yield to maturity calculation is often meaningless. For example, in September 2007, a NoNo issued by Merrill Lynch was selling at a price of $1,157.41, with a yield to maturity of negative 27.66 percent. At the same time, a NoNo issued by Bank of America was selling for $1,511.88, with an implied yield to maturity of negative 169 percent!

Page 15 of 21

15.4 Long-Term Syndicated Bank Loans

15.5 International Bonds

A Eurobond is a bond issued in multiple countries but denominated in a single currency, usually the issuer’s home currency. Such bonds have become an important way to raise capital for many international companies and governments. Eurobonds are issued outside the restrictions that apply to domestic offerings and are syndicated and traded mostly from London. However, trading can and does take place anywhere there are buyers and sellers.

file:///C:/Users/dehartjr/Calibre%20Library/Ross,%20Stephen%20A_/Corporate%20Finan... 5/21/2012

Page 16 of 21

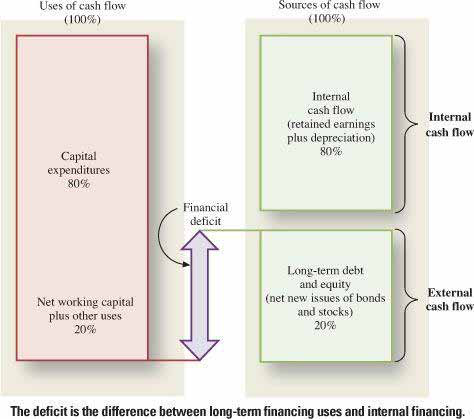

Several features of long-term financing seem clear from the following figures and tables:

1. Internally generated cash flow has dominated as a source of financing.

Page 17 of 21

file:///C:/Users/dehartjr/Calibre%20Library/Ross,%20Stephen%20A_/Corporate%20Finan... 5/21/2012

Page 18 of 21

Figure 15.4 Market Debt Ratio: Total Debt as a Percentage of the Market Value of Equity for U.S. Non-farm, Nonfinancial Firms from 1995 to 2007

file:///C:/Users/dehartjr/Calibre%20Library/Ross,%20Stephen%20A_/Corporate%20Finan... 5/21/2012

However, the use of market values contrasts with the perspective of many corporate practitioners.

Our conversations with corporate treasurers suggest to us that the use of book values is popular because of the volatility of the stock market. It is frequently claimed that the inherent volatility of the stock market makes market-based debt ratios move around too much. It is also true that restrictions of debt in bond covenants are usually expressed in book values rather than market values. Moreover, firms such as Standard & Poor’s and Moody’s use debt ratios expressed in book values to measure creditworthiness.

1. Residual risk and return in a corporation.

file:///C:/Users/dehartjr/Calibre%20Library/Ross,%20Stephen%20A_/Corporate%20Finan... 5/21/2012

3. Preferred stock has some of the features of debt and some of the features of common equity. Holders of preferred stock have preference in liquidation and in dividend payments compared to holders of common equity.

4. Firms need financing for capital expenditures, working capital, and other long-term uses. Most of the financing is provided from internally generated cash flow. In the United States only about 25 percent of financing comes from new debt and new equity. Only firms in Japan have historically relied more on external financing than on internal financing.

3. Preferred Stock Preferred stock doesn’t offer a corporate tax shield on the dividends paid. Why do we still observe some firms issuing preferred stock?

4. Preferred Stock and Bond Yields The yields on nonconvertible preferred stock are lower than the yields on corporate bonds. Why is there a difference? Which investors are the primary holders of preferred stock? Why?

9. Long-Term Financing As was mentioned in the chapter, new equity issues are generally only a small portion of all new issues. At the same time, companies continue to issue new debt. Why do companies tend to issue little new equity but continue to issue new debt?

10. Internal versus External Financing What is the difference between internal financing and external financing?

13. Callable Bonds Do you agree or disagree with the following statement: In an efficient market, callable and noncallable bonds will be priced in such a way that there will be no advantage or disadvantage to the call provision. Why?

14. Bond Prices If interest rates fall, will the price of noncallable bonds move up higher than that of callable bonds? Why or why not?