Define and communicate the benefits and disadvantages newapproaches

Manage finances within a budget

SITXFIN009

This unit describes the performance outcomes, skills and knowledge required to take responsibility for budget management where others may have developed the budget. It requires the ability to interpret budgetary requirements, allocate resources, monitor actual income and expenditure, and report on budgetary deviations.

The skills and knowledge for budget development are covered in SITXFIN010 Prepare and monitor budgets.

Nil

Competency Field

Manage finances within a budget

1.1.2 Functions of financial management ......................................................................... 2

1.2 Budget ................................................................................................................... 3

1.6 Types of budgets .................................................................................................. 7

2 Allocate budget resources ...................................................................... 10

2.1.4 Budget priorities .......................................................................................................... 14

2.2 Discuss changes to income and expenditure priorities .................................. 16

2.4.2 Ways to promote awareness of importance of budget control .......................... 20

2.5 Maintain detailed records of resource allocations ......................................... 21

3.1.1 Financial records ........................................................................................................ 26

3.1.2 Ways to monitor actual expenditure and income ................................................ 27

3.3.1 Deviations or variances ............................................................................................. 30

3.4 Investigate appropriate options for effective management of deviations .. 36

3.4.1 Management of small to mid-size deviations ......................................................... 36

4.1 Assess existing costs and resources ................................................................... 42

4.1.1 Review profit and loss ................................................................................................ 43

4.3.1 Investigate new approaches ................................................................................... 49

4.4 Take account of impact on customer service levels and colleagues .......... 52

5.1 Complete financial and statistical reports within timelines ............................. 56

5.1.1 Financial reports ......................................................................................................... 56

5.2.1 Tips to prepare effective financial reports .............................................................. 65

5.2.2 Do’s and Don’ts in reporting ..................................................................................... 65

1 Introduction

|

|---|

1.1Managing finances

Managing finances or financial management is the process of managing the financial resources of an organisation in order to accomplish the set objectives and goals. It is

1.1.1Importance of financial management Financial management play a key role in-

Planning financial resources

Planning financial resources

Enhancing economic stability

Enhancing economic stability

1.1.2Functions of financial management The main

functions of financial management are –

To provide management with accurate and timely information to help make

planning decision

To provide management with accurate and timely information to help make

planning decision

The financial manager needs to forecast the amount of capital required for business activities like establishment, expansion and modernisation, invest in fixed assets and meet daily working requirements.

f.Monitor financial activities

Finance manager has to be alert at all times about the financial

activities and business position. The manager should continuously

monitor the financial activities of the business.

1.2Budget

A budget is defined as a detailed financial plan that shows estimated

revenue and expenses for a given time period which in turn determines

the profitability of a business.

|

|---|

Figure 3: Budget

A budget forecasts the financial results and financial position of a

company for one or more periods. A budget is used for planning and

performance measurement, which involves spending on fixed assets,

training employees, setting up bonus plans etc.

Figure 4: Financial budget

Budgets are very versatile tools. They can be tailored to suit a wide

variety of situations and levels within an organisation. For example, a

budget could show expected

trading period within any given day.

1.2.1Purpose of budgets

A means to monitor business performance

A means to monitor business performance

1.3Importance of budgeting

Integrating all the activities of organisation

Integrating all the activities of organisation

Communicating the plans to employees at all the levels

Communicating the plans to employees at all the levels

Preparing a budget is a meticulous task. They can be a costly and time-consuming

exercise for a business. It is significant to understand the reasons for budgeting so that

Budgets help to control costs

Budgets help to control costs

Budgets help evaluate business performance

Budgets help evaluate business performance

Assets – Items any business owns

Assets – Items any business owns

Credit worthiness – when a company or an individual has

demonstrated their ability to meet their obligations on time

Credit worthiness – when a company or an individual has

demonstrated their ability to meet their obligations on time

Creditor – a person to whom a company owes money for

the purchase of goods or services

Creditor – a person to whom a company owes money for

the purchase of goods or services

Goods – the movable items bought by a business such as

the stock of food and beverage

Goods – the movable items bought by a business such as

the stock of food and beverage

Liability/ liabilities – a potential loss, financial

obligation, debt or claim of a company or an individual. This is an

obligation that legally binds a company or an individual for the

settlement of a debt.

Liability/ liabilities – a potential loss, financial

obligation, debt or claim of a company or an individual. This is an

obligation that legally binds a company or an individual for the

settlement of a debt.

accounts, the accounts are balanced and based on them the management financial reports are also prepared at this time.

Overdraft - when a lending institution gives an

extension

Overdraft - when a lending institution gives an

extension

Services – the tasks that are performed by businesses

or people. For example, cleaning.

Services – the tasks that are performed by businesses

or people. For example, cleaning.

Utilities – the basic things needed at a workplace.

Example, gas, water, electricity (in case of the hospitality

industry)

Utilities – the basic things needed at a workplace.

Example, gas, water, electricity (in case of the hospitality

industry)

Manage finances within a budget

|

|---|

8

Manage finances within a budget

f.Static budget: Like fixed costs, static budgets are the static expenses, which do not change for a long duration of time. The expenses may include warehouse cost, factory maintenance, supply costs etc.

g.Purchasing budget: A purchase budget is also known as an expense budget, and shows the projected expenditure of the business.

2 Allocate budget resources

Budget resources must be allocated to various activities that helps to generate fruitful profits for the business. Though there are no hard rules for allocation of budget but it is the responsibility of the finance manager of a business to allocate resources as per the budgeted priorities.

Manage finances within a budget

Sales and marketing

Sales and marketing

Operations

Operations

Developing a budget includes determination of level of resources required for the business to operate and the expenditure limits for each category.

2.1.1Budget formats

Manage finances within a budget

Size of the business does not affect the budget allocation and the usage, as every business needs to prepare budgets as per their priorities. There exists no specific rule for allocation of funds, it completely depends on the nature of the business and its dealings in the market.

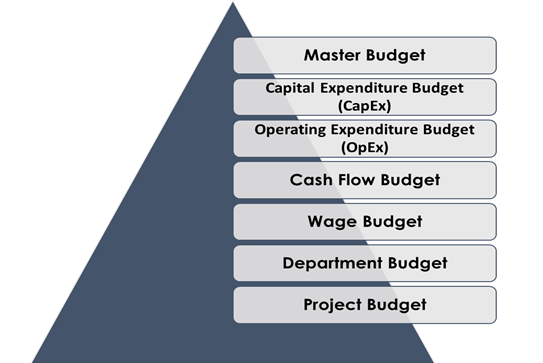

Based on the size and nature of the dealings, business select appropriate format and type of budget. Small businesses use master budgets, as it combines all the budgets in one clear format and provides organised information for easy analysis. Whereas medium to large businesses prepare different budgets based on the need.

A calendar year (1st January to 31st December)

A calendar year (1st January to 31st December)

A corporate financial year (1st October to 30th September).

A corporate financial year (1st October to 30th September).

allocated to budgets on an annual basis, the cycle covers the costs or expenditures for a specific year.

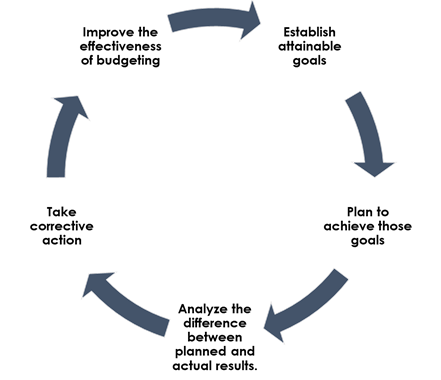

The steps involved in budget cycle are:

|

|---|

Once established the goals, it is necessary to develop a master budget, which aims to move the business towards achieving the established goals. Based on how the funds have been allocated, the Operational, sales, expenditure, financial and other budgets are developed in the master budget. While making these budgets, ensure to set targets that are attainable and within reach of the staff’s responsibilities.

3.Analyse the difference between planned and actual results

variance should be reported for any necessary action to improve the overall performance.

4.Take corrective action

Each business has its own mode of operations by virtue of which it may choose to focus on short term or on long term goals. Priorities vary from business to business and

14

Figure 8: Budget priorities

Some of the general priorities include:

Activities to sustain competition

Activities to sustain competition

While allocating funds, one should-

Allocate funds by department wise

Allocate funds by department wise

Consider the external factors that affect budgets and fund

allocation-

Consider the external factors that affect budgets and fund

allocation-

15

Manage finances within a budget

2.2Discuss changes to income and expenditure priorities

Once the funds get allocated, it is necessary to discuss the changes in the income

Budgeting professionals

Budgeting professionals

Supervisors from relevant departments

Supervisors from relevant departments

The changes in income and expenditure priorities may be due to changing market

conditions, competitor actions and other factors. The factors must be analysed and

2.2.1Tips to manage changes in priorities

Based on the changes in the priorities, one should manage the changes effectively

Organise the tasks based on the changed priorities

Organise the tasks based on the changed priorities

Set monitoring controls

Set monitoring controls