3.2 accounting for revenue from contract with customers

ACCOUNTING THEORY AND APPLICATION

Student Name:

6 May 2020

To

Sydney NSW 2000

By Email: procurement@asic.gov.au

Mr A. Morris, Chair, Consultant Committee, Success Consultancy on (T) 45879535 or at (E) a.morris@scgmail.com

Mr C. Black, MD, Consultant Committee, Success Consultancy on (T) 87945624 or at (E) c.black@scgmail.com

The study has been conducted with the key aim of evaluating the compliance, and applicability of the standards that have been highlighted by AASB on the Australian companies. This has been conducted by provided special reference to Apiam Animal Health Limited for meeting the purposes of the study. It is a healthcare-related company based on the health of the pet and domestic animals and having its operations in Australia. This report focuses on the implication and compliance of the relevant accounting standards according to the operations of the said company as seen from its annual report of 2019. They have been recognized based on its operations and the financial notes that have been provided in the annual report. The key highlights of accounting standards that can be seen are AASB 9 dealing with financial instruments, AASB 15 dealing with the revenues from the contract with customers, and AASB 16 dealing with lease accounting. All of them have been emphasized in the current study regarding their individual usage for the accounting process of the said company.

The study sheds light on the use of AASB 9 for managing and measuring its financial statement that can enrich its financial worthiness, which is also relevant for AASB 16. Regarding AASB 15, the study deals with compliance of better management for Apiam so that effective customer relationships can be managed in its market. With the application of the mentioned standards, Apiam can comply with an effective business management system as it will be legally correct in all respects. Regarding this, it is essential for Apiam in following all the guidelines as mentioned by these standards for better management of its financial statements. Moreover, they are required in increasing its financial efficiency and stability by providing a legal and appropriate view of its reports to its key stakeholders. They can provide appropriate support to this company in the future regarding different business points of view.

2.1 AASB 9- Accounting for Financial Instruments 9

3.1 Accounting for Financial Instruments 12

3.1.1 Compliance with AASB 9 13

3.2.3 Earnings Management for Accruals 19

3.2.4 Earnings Management for Measurement 20

4.1 Implication of AASB 9 on Apiam 26

4.2 Implication of AASB 15 on Apiam 27

List of Figures

Figure 1: Balance of Retained Earnings 17

1. Introduction

The provided report is conducted to identify and analyze the guidelines of AASB if they have been compiled by Apiam Animal Health Limited, which is an Australian company. It is effective in ensuring the financial reflections of this company that is being made in association with the accounting guidelines for special cases, such as leases and financial instruments. With this, the applicability status of this company regarding the rules of AASB can be analyzed, which can help to analyze the managerial activities of Apiam along with corporate governance, and remunerations policies. The study chooses to perform the analysis on the basis of the annual report of the concerned company for the year 2019. The report is mainly prepared for analyzing Apiam's compliance with the required AASB guidelines so that the report can be presented before ASIC (Australian Security Investment Commission) for further consideration. Hence, the report is also effective in evaluating the financial impacts on the reports and performance of Apiam by following the practices of AASB.

2. Methodology

AASB 9- Accounting for Financial Instruments

AASB 15- Accounting for Revenue from Contract with Customers

2.1 AASB 9- Accounting for Financial Instruments

| 2019 | 2018 | 2017 | 2016 | |

|---|---|---|---|---|

| Operating cash flow ratio | 4,884/18,785 | 9,217/21,446 | 1,670 /17,641 | 1,237/19,708 |

| Debt ratio | 43137/104446 | 46679/105404 | 39921/94403 | 31815/78086 |

(Source: apiam.com.au, 2019)

2.2 AASB 15- Accounting for Revenue from Contract with Customers

The accounting processes for the revenues that are extracted from the contracts entered by Apiam with its customers are monitored under AASB 15, which governs such revenues under the eyes of AASB. These are the factors associated with the contracts made regarding providing veterinary services throughout the country, which is completed by the concerned company by highlighting revenue recognition models and other relevant facts associated with this. Thesis standards are most appropriately required for those companies that are having various contracts with their external customers. AASB 15 is a completely new framework that has been brought to light by the accounting board of the country for relevant maintenance of the revenues from such contracts. With the use of this standard, the stipulated timing and concerns of recording them in an appropriate manner can be evaluated so that they can be associated with relevant financial disclosure for the key users of reports.

2.3 AASB 16- Accounting for Leases

2.4 Limitations of the Research

3. Findings

The findings portion of the provided report concerns the observations seen in the report of Apiam in association with the three identified AASBs as per its operations. These are retrieved from the annual financial statements of this company along with the associated financial notes as required for considering each of the identified AASBs. Hence, this portion of the study focuses on analyzing and evaluating the ways that have been applied by Apiam in following the guidelines of AASB according to the application of the three standards, which have been conducted from its annual report of 2019.

3.1 Accounting for Financial Instruments

3.1.1 Compliance with AASB 9

Figure 1: Balance of Retained Earnings

(Source: apiam.com.au, 2019)

3.1.2 Financial Reporting for Investors

Figure 2: Share Price of Apiam

| 2019 | 2018 | 2017 | 2016 | ||

|---|---|---|---|---|---|

| Operating Cash flow/Current liabilities | |||||

| Operating cash flow ratio | 0.26 | 0.43 | 0.09 | 0.06 | |

| Total Liabilities/Total Assets | |||||

| Debt ratio | 0.41 | 0.44 | 0.42 | 0.41 | |

| Current Assets-Inventories/Current Liabilities | |||||

| Liquidity ratio | 0.89 | 0.79 | 0.90 | 0.80 |

Table 3: Ratios for Investors

(Source: apiam.com.au, 2019)

3.2 Accounting for Revenue from Contract with Customers

Recognizing the contracts that have been entered into with then customers

Identifying the obligations required for executing such contracts

3.2.1 Compliance with AASB 15

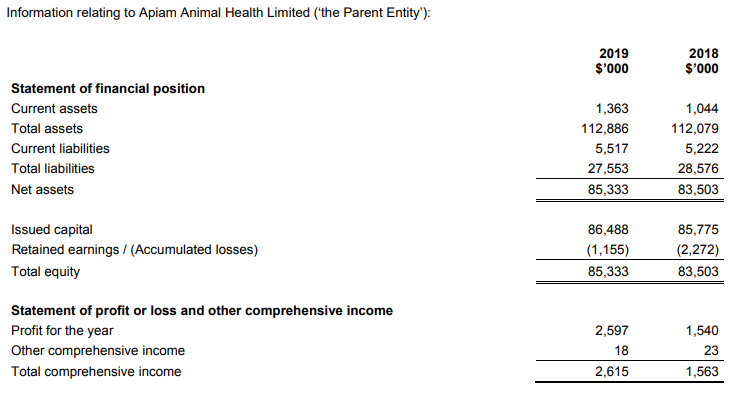

The compliance of Apiam with AASB 15 can be evaluated from its annual report, which identifies that the company has been using this standard in place of AASB 118 and 111 considering the accounting for revenue and construction contracts respectively. The new standard of AASB 15 has been applied by Apiam from 1 July 2018 through the use of a modified retrospective approach (apiam.com.au, 2019). Hence, with the use of this method, the said company has recognized the cumulative effects of its initial application for making necessary adjustments. These adjustments have been highlighted by Apiam in the opening balance of its retained earnings with the effect from 1 July 2018. Regarding this, Apiam has also mentioned that the adjustments that have been made for the revenues it has earned from the contracts made with its customers are applied in the form of retained earnings balance (apiam.com.au, 2019). Hence, for this, the adoption of this standard did not provide any material impact on the financial transactions of Apiam along with the balances as seen in its financial statements.

3.2.2 Remuneration

Remunerations of the members in the board and the management team of Apiam have been outlined in its remuneration report that makes arrangements according to the requirements of the Corporations Act 2001. It defines the responsibilities of the key management personnel in this company who are having all the authority and responsibilities of directing, planning, and controlling the operations of Apiam. It consists of six directors, among whom one director named Charles Sitch has resigned on 29 November 2018 (apiam.com.au, 2019). Another director named Jan Tennent was appointed by the board on 1 August 2018, which indicates that there exists the relationship of agent and principal in the company. It relates to the agency theory, which means that the directors are the agents working on behalf of the boards for the betterment of Apiam. Among the other directors, Andrew Vizard is the Chairman and non-executive, Chirs Richards is the MD and executive director, Micheal Blommestein and Richard Dennis are non-executive directors and Matthew White is the CFO of Apiam (apiam.com.au, 2019). All of them are responsible for company activities. The economic assumptions, in this case, can be seen in the rational economic views suggesting that the people in any organization act to maximize personal benefits for increasing financial wealth. It can be highlighted from the remuneration circulation in Apiam among its board members.

The Listing Rules and Constitution that has been provided in the ASX allows Apiam to increase all the aggregate amounts provided for remuneration payable to its non-executive directors (apiam.com.au, 2019). No STI has been included by Apiam till date in the remuneration package of any of its board members that can be seen in the report. Moreover, its remuneration framework is seen to be competitive to the market and complementary to its reward strategies.

3.2.3 Earnings Management for Accruals

The earnings management for any company is effective in influencing costs connected with STI for the formation of accrual accounting. The formula provided by DeAngelo can be used in measuring such accruals that may include provisioning of bad debt, altering estimates of depreciation, delaying impairment of assets, and adjusting the inventory values (DeAngelo, 1986). It can also be used for Apiam in managing its accrual earnings by procuring the required data from its annual report. DeAngelo's formula can identify all the accounting accruals indicating effective management of such accruals.

Table 4: Accrual Differences

(Source: apiam.com.au, 2019)

3.2.4 Earnings Management for Measurement

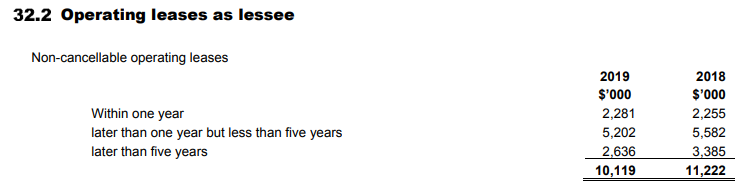

3.3 Accounting for Leases

Some issues were developed due to the use of AASB 117 due to the differences that are seen in the two types of leases. Hence, this was replaced by AASB 16 that was a more modified version and can be effectively used for differentiating the leases (pwc.com, 2016). This was effective from July 2019, which will require the leases having the contract term of 12 months to be recorded in the balance sheet of individual companies with the account of lease liabilities (aasb.gov.au, 2020). The associated expenses will be included in the income statements of the companies, which can also be seen in the accounts of Apiam.

3.3.1 Compliance with AASB 16

AASB highlights accounting for leases in standard number 16 that has been seen in the reports of Apiam, thus reflecting that this company has been using these standards since its incorporation. Leases are associated with both assets and liabilities of the said company, which are being measured through the use of their present values maintained by Apiam. Its report also highlights AASB 117 that has been recently replaced by AASB 16 by making some modifications in the old one (apiam.com.au, 2019). Regarding this, Apiam mentioned in its reports that the company has been using AASB 16 by making it effective since 1 January 2019, before which it used to comply with the guidelines provided in AASB 117 (aasb.gov.au, 2016). The financial notes of Apiam highlight its compliance with this accounting standard, which has been replaced for AASB 117. According to the company’s compliance, this new standard will require all the leases to be recorded in the on-balance sheets of every lessee excluding low valued assets and short-term leases. It also provides different types of guidance for the application of the lease definition in that of Apiam along with its leaseback and sale accounting. Furthermore, AASB 16 is effective for Apiam by providing different and new disclosing techniques for its leases.

Figure 3: Financial Lease of Apiam

Figure 4: Operating Lease of Apiam

(Source: apiam.com.au, 2019)

Figure 5: Cash Flow Statements

3.3.2 Corporate Governance

The directors along with the management of Apiam are seen to comply with the highest standards of its corporate governance along with maintaining ethical manners. The adoption of this by Apiam has been maintained according to the sustainability compliance with the ASX Corporate Governance Principles and Recommendations so that they can be effective in its operations (apiam.com.au, 2019). According to the highlights of its corporate governance, the board is seen to have eight principles in it, which is followed by the company throughout the financial year. The first principle in its governance entitles a layout bringing a solid foundation for its management, which mentions establishing and disclosing all the roles and responsibilities of the board and management of Apiam along with the ways of monitoring and evaluating their performance. The second principle focuses on the structure of the board so that it can add value to the company. It says that Apiam must have a board with appropriate composition, size, commitments, and skills so that they can be able to discharge their individual duties effectively (apiam.com.au, 2019). The third principle of its governance says the application of responsible and ethical acts of the board and management, which must be associated with its code of conduct.

The fourth principle focuses on safeguarding integrity in the ways of its corporate reporting, which means that Apiam must have rigorous and formal processes that can be helpful in safeguarding and verifying the integrity of the corporate reporting independently. The fifth principle is associated with making a balanced and timely disclosure of all the matters that are associated with having material impacts on the value or price of Apiam's securities (apiam.com.au, 2019). Respecting the rights and authorities of the security holders of Apiam has been highlighted in the sixth principle, which requires the company to provide its security holders with all appropriate and required information and facilities that will help them in exercising their rights. Recognizing all the possible risks and managing them through effective risk management have been included in the seventh principle of its governance, which will be done by a framework with its periodical review for maintaining effectiveness. The last or the eighth principle discusses a responsible and fair remuneration policy for the directors that will be required for attracting and retaining qualified directors (apiam.com.au, 2019). It also maintains sufficient remuneration required for the senior executives so that they can be attracted, retained, and motivated for aligning their interests with value creation for security holders.

4. Implication of Findings

4.1 Implication of AASB 9 on Apiam

Impairment: It is required for Apiam in recognizing its potential losses that will be according to the use of its model for expected credit losses (Stebbens, 2017). This will ensure the doubtful debt provisions accounting for its potential losses.

The measurements of and accounting for the financial instruments have become simplified as compared to the previous ones that have been effective for Apiam in measuring them. It is seen to measure its instruments at fair value that has been recognized in its comprehensive income statement. According to the statements of Apiam, it will be required to assess its credit risks in a broader sense along with the expected credit losses (apiam.com.au, 2019). It reveals that Apiam is exposed to such risks from its financial assets including its cash held at bank and the trade receivables. It is based on the historical information of the trade receivables as they are spread over a vast geographical area, which can create default rates among customers. Hence, this provides a hint that Apiam must require a provision of trade receivables that will be applicable under AASB 9 (apiam.com.au, 2019). It does not provide any provision for omitting the doubtful debt records for any company so that this can help recognize any expected losses in the future. It will be required for Apiam in addressing the same in its upcoming reports. Hence, though Apiam is seen to appropriately company with the requirements of AASB 9, some more requirements will be required in its reports for further improvements.

4.2 Implication of AASB 15 on Apiam

4.3 Implication of AASB 16 on Apiam

| 2019 | 2018 | 2017 | 2016 | ||

|---|---|---|---|---|---|

| Debt to Equity ratio | |||||

| Operating lease expensed | Total liabilities/Total equity | 0.704 | 0.795 | 0.733 | 0.688 |

| Operating lease capitalized | Total liabilities+Operating Lease expenses/Total equity | 0.715 | 0.806 | 0.740 | 0.694 |

| Debt ratio | |||||

| Operating lease expensed | Total liabilities/Total assets | 0.413 | 0.443 | 0.423 | 0.407 |

| Operating lease capitalized | Total liabilities+Operating lease expenses/Total assets | 0.420 | 0.449 | 0.427 | 0.411 |

The reduction of its debt ratio from the previous year says that Apiam is keen on reducing its liabilities due to the use of accounting for leases. From its reports, it is seen that Apiam is using the previous leases standards for complying with the lease accounting (apiam.com.au, 2019). However, this is also influencing its ratios, as following the previous standard is also creating lease liabilities for the company by dividing them into financial and operating leases. It has made duly allocation of the expenses payments on the cash flow statement of Apiam. Regarding the debt ratios, they can be seen decreasing for both debt and debt to equity ratios from 2018 to 2019. This is relevant for both charging the operating leases as expenses and as capitalized forms. Hence, it can be said that Apiam's decisions regarding the non-adoption of the new standard at the earlier stage may be associated with its priority of reducing its overall debts.

According to the report of 2019, the management of Apiam is planning to implement AASB 16 with its effects from 1 January 2020, which will have its effects and outcomes in the report of 30 June 2020 (apiam.com.au, 2019). This will have materials impacts on its balances and transactions that will be recognized in its financial statements in the next accounting year. The impacts, as mentioned by Apiam, will be as follows:

It is hence evident from its reports that Apiam has declared correctly regarding its compliance with AASB 16 along with the changes that it will be having in its accounting process. It will be an important goal for Apiam in targeting the required segments of leases for making appropriate financial predictions in the future years, which can ensure its stable financial situations.

5. Conclusion and Recommendations

AASB 16- Accounting for Leases

Regarding this, it can be noted that other standards do not comply with the current operations and business requirements of Apiam. Apart from this, some important things have been noticed in its reports. Its annual report highlights the mentions of Grant Thornton, the independent auditor of Apiam that it requires using the standard for impairment of assets for the assets that can be impaired. However, it can be seen that initially Apiam is not providing for these standards and may provide this in the reports of the upcoming years. Its auditor company has highlighted in its declaration that Apiam is required to assess for these standards, which is AASB 136 for the Impairment of Assets if the company identifies any impairment indicators in its assets. This is mostly applicable for its goodwill, which can help in accessing if the current value of this is exceeding the recoverable value.

With the provided recommendations, it can be effective for Apiam in meeting all the required obligations that will be appropriate for making effective compliance with the said accounting standards. Hence, the current investigation of its compliance with the extracts from its annual report highlights some important facts. The study highlights not only the compliance that is required for a company to be made regarding the appropriate accounting standards; however, it also says the practices that will have positive accounting on a company. It is also evident that the management of Apiam has acted appropriately for reducing its dents in the current year so that positive impacts can be witnessed in the upcoming years. It is associated with profit enhancement, which is required for paving ways for development and prosperity in the future years.

Reference List

aasb.gov.au, (2016). Leases Retrieved from: https://www.aasb.gov.au/admin/file/content105/c9/AASB16_02-16.pdf

allanhall.com.au, (2020). Application of the Updated Lease Accounting Standard – AASB 16: What You Need to Know as a Business Retrieved from: https://allanhall.com.au/aasb-16-leases-what-you-need-to-know/

apiam.com.au, (2016). Annual Report 2016 Retrieved from: https://www.apiam.com.au/wp-content/uploads/2017/09/apiam-animal-health-2016-annual-report.pdf

apiam.com.au, (2020). About Retrieved from: https://www.apiam.com.au/about/

apiam.com.au, (2020). Our values Retrieved from: https://www.apiam.com.au/locations-diversity/

deloitte.com, (2020). IFRS 9: Financial Instruments.

Retrieved from:

https://www2.deloitte.com/content/dam/Deloitte/ru/Documents/audit/ifrs-9-financial-instruments-en.pdf

Fargher, N., Sidhu, B. K., Tarca, A., & Van Zyl, W. (2019). Accounting for financial instruments with characteristics of debt and equity: finding a way forward. Accounting & Finance, 59(1), 7-58.

Stebbens, P. (2017). AASB 9 Financial Instruments – Transitioning: Practical guide Retrieved from: https://home.kpmg/au/en/home/insights/2017/09/aasb-9-financial-instruments-transition-practical-guide.html

Wang, X. (2016). An Empirical Investigation into Compliance by Australian Firms with the Disclosure Requirements of International Financial Reporting Standards.