Financial Statements in Accounting Assignment Help

Definition of financial statements

It is the outline reports that show how a company has used the assets depended on it by its lenders, shareholders, and stockholders, and what is the contemporary financial status (Lunt, 2006).

Purpose of financial statements

These are a bunch of reports of an association's financial status, financial returns, and flows of cash.

Importance of Financial statements

- Importance of these statements are to:

- Choose the boundary of a company to make the sources and the capital and livelihoods of that cash.

- Track if a business can remunerate its commitments.

- Follow the financial outcomes on a model line, to identify any rising issues of profitability.

- Get financial limits from the reports that can explain the status of the company.

- Analyse the purposes of enthusiasm of specific market trades, as outlined in the presentations that work with the declarations.

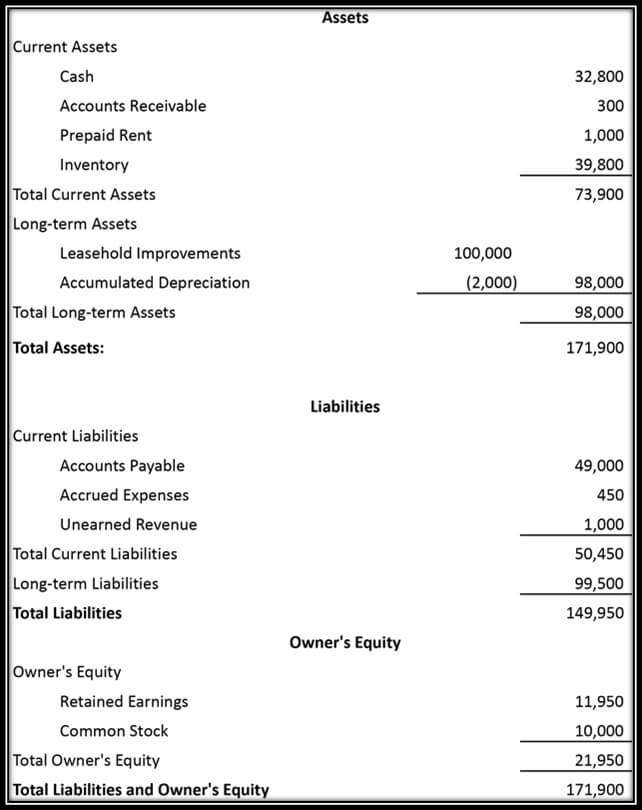

The Balance Sheet

Purpose of the balance sheet

It is a statement that condenses the majority of an item's benefits, compulsions, and purpose within the given period. Loan lenders ordinarily utilize it. Then investors and creditors are also there to assess the liquidity of a trade. It is a component of the reports combined into a substance's financial statements. In the finance statement, this sheet is expressed as of the end of the reporting period, while the cash flow and income statement cover the whole reporting season (Harris and Mongiello, 2006).

Components of balance sheet

The components of balance sheet are:

Equity

Liabilities

- Current Liabilities

- Long-term Liabilities

Assets

- Current Assets

- Long-term Assets

- Other Assets

Financial Statements in Accounting Assignment Help By Online Tutoring and Guided Sessions from AssignmentHelp.Net

Format of balance sheet

Figure 1: Account Format

Figure 2: Report Format

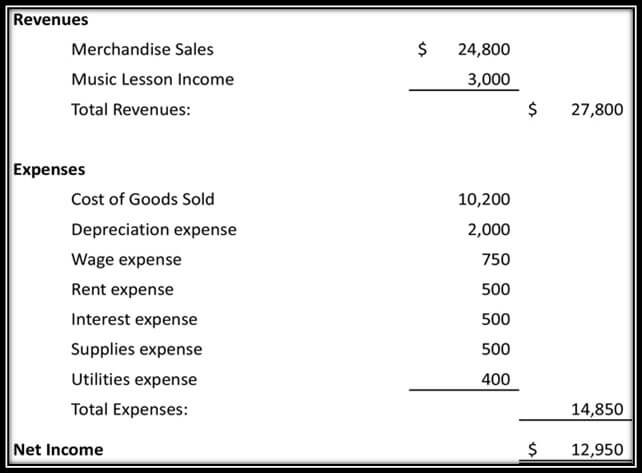

Income Statement

Purpose of Income Statement

It is a financial statement that demonstrates an element's financial results over a specific period. The period is secured as per period for a year, quarter, and month. Then again, it is possible that partial periods may similarly be used. It is the most generally used of the financial reports and is the probable explanation to be divided within a business for organizational survey.

Components of Income Statement

Single-step income statement: It just demonstrates to one class of pay and one classification of costs. This organization is less helpful to outside clients because they cannot figure numerous effectiveness and benefits proportions with this constrained information.

Multi-step income statement: It isolates cost accounts into more important and usable records given their capacity. Expense of merchandise sold, working and non-working costs are isolated out and used to compute gross benefit, working salary, and net wage.

Format of Income Statement

Figure 3: Income Statement

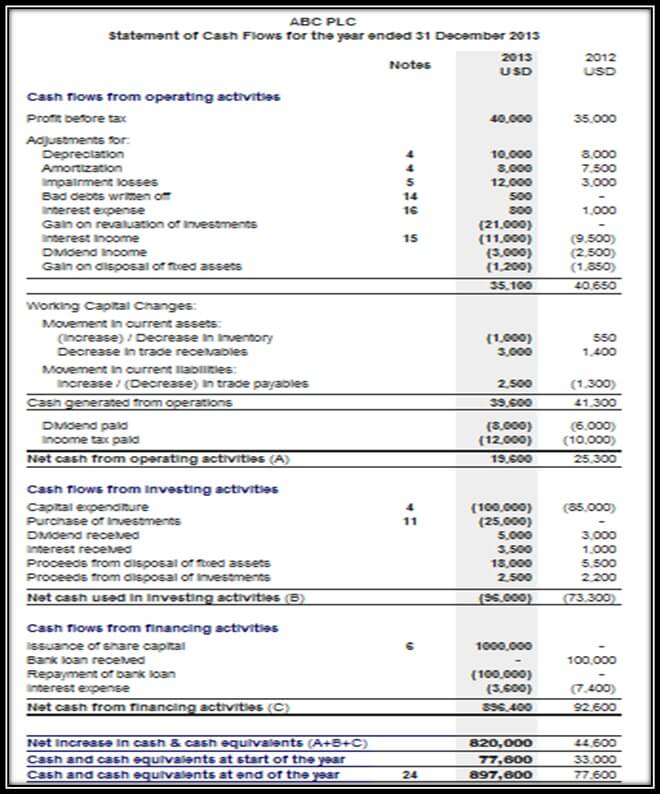

The Statement of Cash Flows

Purpose of Cash Flow Statement

As the wage statement is readied under the gathering premise of accounting, the incomes reported might not have been gathered. Additionally, the costs gave an account of the pay statement will not have been paid. A user could survey the monetary changes to decide the actualities, yet the income statement as of now has incorporated all that data. Accordingly, skilled specialists and stockholders use this essential financial statement (Libby, Libby and Short, 1998).

Format of the cash flow Statement

The format of the cash flow statement is as follows:

- Operating Activities

- Investing Activities

- Financing Activities

Examples of Cash Flow Statements

Figure 4: Example of the Statement of Cash Flows

The Purpose of Notes on Financial Statements

It is to give an important portrayal of the things displayed in the essential financial statements and of unrecognized game plans, claims against and privileges of the substance that exist at the reporting date. Notes for the financial statements report the points of interest and extra data that are let alone for the principle reporting records, for example, the monetary record and pay statement. It is done essentially for the purpose of clarity because these notes can be very long, and on the off chance that they were incorporated; they would cloud the information reported in the financial statements (Pratt, 2000).

It is critical for stockholders to peruse the notes to the financial statements incorporated into an association's aristocracy records. These notes include basic information on such things as the bookkeeping methods of insight used for recording and reporting trades, advantages plan unpretentious components, and venture opportunity compensation information - all of which can be valuable impact on the primary issue that a shareholder can envision from an enthusiasm for an association.

Preparing the Basic Income Statement and Statement of Retained Earnings

The first prepared statement is known as "Income Statement". Total income is the total of all the cash that has been acquired by an organization an accounting period. Cumulative costs are the total of all cash that was paid out by the organization. Net income comes if all income surpasses absolute costs. Net loss comes when the aggregate costs are more than aggregate income (Revsine, 2009).

It follows the following formula:

Total Income - Total Expenditures = Net Income/ Net Loss

Next, the prepared financial statement is known as the “Statement of Retained Earnings.” The term "retained earnings" alludes to the measure of net salary that is left in an organization after profits have been paid to shareholders if there are any, and after the proprietor has pulled back cash for himself. It follows the following formula:

OR

Starting Retained Earnings - Net Loss - Withdrawals of Dividends or Owner's = Final Retained Earnings

Preparing the Basic Balance Sheet and Statement of Cash Flows

The balance sheet is prepared third in the financial statement. It incorporates the last balance of each of the components recorded in the accounting analytical statement. The 'ending retained earnings balance' continues from the retained earnings statement to the accounting report.

Cash flow is the last statement in income statement format. It clarifies the utilization of money for the three cash flow classes:

- Investing Activities

- Operating Activities

- Financing Activities

Toward the end of the announcement, the net increment or depreciate in existing money is indicated accommodating the starting money parity to the closure money equalization provided details regarding the individual monetary record (Weygandt, Kieso and Kimmel, 2003).

External Audits of Financial Statements

It is an autonomous review of the financial statements arranged by the company. It is normally led for statutory purposes. It can be directed either to a major aspect of the yearly survey of records or as an exceptional audit by a provider organization. It is directed by an enrolled firm of financial analysts with perceived proficient capabilities. The reason for this review is to check that the yearly records give a genuine and reasonable image of the company’s finances and that the utilization of assets is as per the points and protests as laid out in the constitution. It is not the prime part of the review to identify misrepresentation, in spite of the fact that this might obviously become known amid the watches that happen (Revsine, 2009).

The Fundamental Principles of Accounting

Accounting’s fundamental principles are (Stittle and Wearing, 2008):

Financial Unit: Accounting needs all qualities to be recorded as far as a solitary financial unit. It can't represent products like the bargaining framework.

Working Concern: This rule infers that the firm will keep on doing its nothing new until the end of the following accounting period and that there is no data despite what might be expected.

Conservatism principle: It can be found in the way that financial analysts esteem stock at lower of expense or advertise cost.

The principle of cost: It advocates that organizations ought to list everything on the financial statements at the expense cost.

References and Books for Further Reading on Financial Accounting

Harris, P. and Mongiello, M. (2006). Accounting and financial management. Amsterdam: Elsevier/Butterworth-Heinemann.

Libby, R., Libby, P. and Short, D. (1998). Financial accounting. Boston: Irwin/McGraw-Hill.

Lunt, H. (2006). Fundamentals of financial accounting. Amsterdam: Elsevier.

Pratt, J. (2000). Financial accounting in an economic context. Cincinnati, Ohio: South-Western College Pub.

Revsine, L. (2009). Financial reporting and analysis. Boston: McGraw-Hill Irwin.

Stittle, J. and Wearing, B. (2008). Financial accounting. Los Angeles: SAGE Publications.

Weygandt, J., Kieso, D. and Kimmel, P. (2003). Financial accounting. New York, NY: Wiley.