Introduction to Microeconomics

What economics is all about?

Alfred Marshall in his famous textbook on economics, Principles of Economics defined economics as "A study of mankind in the ordinary business of life; it examines that part of individual and social action which is most closely connected with the attainment and with the use of the material requisites of wellbeing. Thus it is on one side a study of wealth; and on the other, and more important side, a part of the study of man." Economics is the science of examining, how people choose limited / scarce resources to fulfill their unlimited desires / wants.

Microeconomics is the branch of economics concerned with decisions made by individual in the economy that tries to explain the behaviour of individual economic agents (the consumers and the producers)

Subject matter of economics

The central theme in all the above and other existing definitions of economics forms the subject matter of economics remain Scarcity of resources and the behaviour of individuals facing scarcity. In the absence of scarcity, economics would not have existed; in fact there would be no need for it

The scope of economics thus encompasses the following:

- Resources: all things used to satisfy human needs directly or indirectly

- Scarcity: non availability of enough resources to satisfy all people needing it

- and Allocation: distribution of scarce resources

Economics: The social science that seeks to understand the choices people make in using scarce resources to meet their wants.

Factors of Production: The basic inputs of labor, capital, and natural resources used in producing all goods and services.

Macroeconomics: The branch of economics that studies large-scale economic phenomena, particularly inflation, unemployment, and economic growth.

Scarcity: A situation in which there is not enough of a resource to meet all of everyone’s wants.

The four basic economic choices include

- What to Produce

- How to produce it.

- For whom to produce it.

- When to produce it.

The Question not included in economic choices is who will produce it.

Labor: The contributions to production made by people working with their minds and muscles.

Economic Efficiency: A state of affairs in which it is impossible to make any change that satisfies one person’s wants more fully without causing some other person’s wants to be satisfied less fully.

Capital: All means of production that are created by people, including tools, industrial equipment, and structures.

Opportunity Cost: The cost of a good or service measured in terms of the forgone opportunity to pursue the best possible alternative activity with the same time or resources.

The difference between out-of-pocket costs and opportunity costs in Applying Economic Ideas is the forgone income

Efficiency in Distribution: A situation in which it is not possible, by redistributing existing supplies of goods, to satisfy one person’s wants more fully without causing some other person’s wants to be satisfied less fully.

Entrepreneurship: The process of looking for new possibilities – making use of new ways of doing things, being alert to new opportunities and overcoming old limits.

Comparative advantage: The ability to produce a good or service at a relatively lower opportunity cost than someone else.

Efficiency in production: A situation in which it is not possible, given available knowledge and productive resources, to produce more of one good without forgoing the opportunity to produce some of another good.

Positive Economics: The area of economics that is concerned with facts and the relationships among them.

Model: A synonym for theory; in economics, often applied to theories that are stated in graphical or mathematical form.

Theory: A representation of the way in which facts are related to one another.

Normative Economics: The area of economics that is devoted to judgments about whether economic policies or conditions are good or bad.

Adam Smith coined the term, “the invisible hand”

Econometrics: The statistical analysis of empirical economic data.

Production Possibility Frontier: A graph that shows possible combinations of goods that can be produced by an economy given available knowledge and factors of productions.

Conditional Forecast: A prediction of future economic events in the form “If A, then B, other things being equal.”

Slope: For a straight line, the ratio of the change in the y value to the change in the x value between any two points on the line.

Direct Relationship: A relationship between two variables in which an increase in the value of one variable is associated with an increase in the value of the other.

Positive Slope: A slope having a value greater than zero.

Negative Slope: A slope having a value less than zero.

Inverse Relationship: A relationship between two variables in which an increase in the value of one variable is associated with a decrease in the value of the other.

In 2016, the unemployment rate for people with no high school diploma was 7.34%

Law of Demand: The principle that an inverse relationship exists between the price of a good and the quantity of that good that buyers demand, other things being equal.

Demand: The willingness and ability of buyers to pay a price for purchasing a specific goods and services in the market.

Supply: The willingness and ability of sellers to provide goods for sale in a market

Demand Curve A graphical representation of the relationship between the price of a good and the quantity of that good that buyers demand.

Change in Quantity Demanded: A change in the quantity of a good that buyers are willing and able to purchase that results from a change in the good’s price, other things being equal; shown by a movement from one point to another along a demand curve.

Change in Price: An increase or decrease in the price that must be paid in order to purchase any specific goods and services in the market.

Change in quantity: An increase or decrease in the amount of a specific goods and services being bought and sold.

Change in demand: A change in the quantity of a good that buyers are willing and able to buy that results from a change in some condition other than the good’s price; shown by a shift in the demand curve.

Change in tastes: A change in the behavior, desires, preferences or habits of consumers that can affect their ability and willingness (demand) to buy particular goods and services in market. This is shown by a shift in the demand.

Supply Curve: A graphical representation of the relationship between the price of a good and the quantity of that good that sellers are willing to supply.

Inferior Good: A good for which an increase in consumer incomes results in a decrease in demand.

Normal Good: A good for which an increase in consumer incomes results in an increase in demand.

Substitute Goods: A pair of goods for which an increase in the price of one results in a decrease in demand for the other.

Complementary Goods: A pair of goods for which an increase in the price of one results in an increase in demand for the other.

Price effect: A change in consumer’s optimal consumption bundle, hence a change in the quantity purchased of a good that results from a change in the price of that good alone, price of all other goods and consumer’s income remaining constant.

Taste effect: A change in consumer’s demand for a specific good and service caused by a change in the habits or preferences, while price of the good remains the same. This is shown by the shift of the demand curve.

Income effect: A change in consumer’s optimal consumption bundle causes by a change in consumer’s income leading to a change in quantity purchased of all goods and services, while prices of all goods and services remain same.

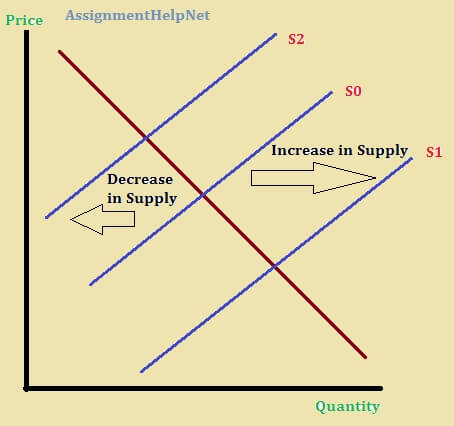

Change in Supply: A change in the quantity of a good that suppliers are willing and able to sell that results from a change in some condition other than the good’s price; shown by a shift in the supply curve.

Inventory: A stock of a finished good awaiting sale or use.

Change in Quantity Supplied: A change in the quantity of a good that suppliers are willing and able to sell that results from a change in the good’s price, other things being equal; shown by a movement along a supply curve.

Equilibrium: A condition in which buyers’ and sellers’ plans exactly mesh in the marketplace, so that the quantity supplied exactly equals the quantity demanded at a given price.

Shortage: A condition in which the quantity of a good demanded at a given price exceeds the quantity supplied. This is the condition of excess quantity demanded.

Equilibrium: A condition in which the quantity of a good supplied at a given price is exactly equal to the quantity demanded.

Surplus: A condition in which the quantity of a good supplied at a given price exceeds the quantity demanded. This is also the condition of excess quantity supplied.

The Graph below illustrates a supply shift

- Factors that can contribute to higher prices, Ceteris Paribus: increase in demand or decrease in supply

- Price support results in surplus

- A price ceiling results in shortage

- Marshall studied Math at St. John’s College, University of Cambridge.

Microeconomics Study Guide

Microeconomics | Microeconomics Help | Introduction To Microeconomics | Microeconomics Theories | Microeconomics Study Guide | Principle Of Microeconomics | Economics Course | Articles On The Economy | Online tutoring